Irritability is important from a mental health perspective as a common symptom of concern and predictor of outcomes.

Answer:

First 4 subparts are answered below:

A)

Equation for budget constraint: p1.x1 + p2.x2 = M

Substituting the given information gives: 1B + 5P = 20

B)

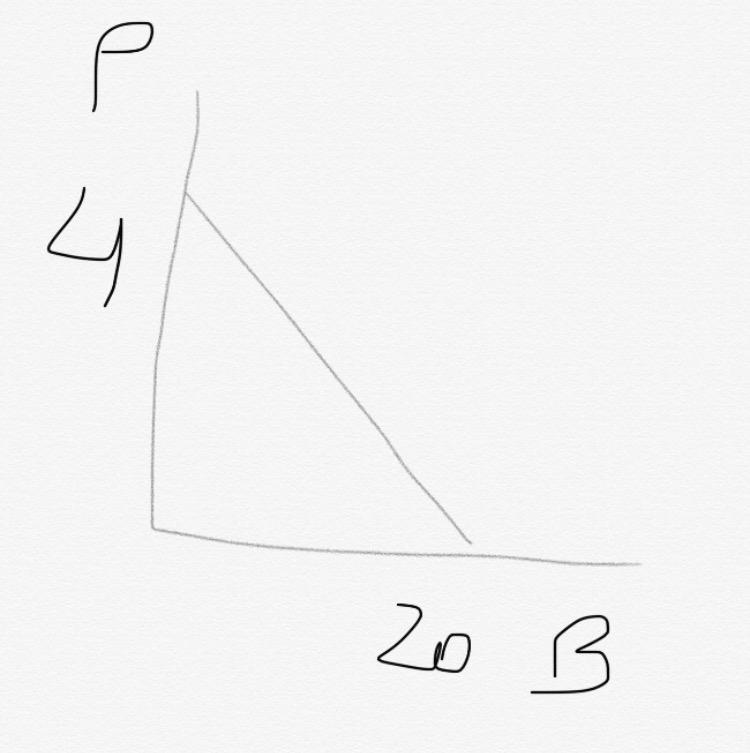

The budget constraint is below: See attachment

C)

Slope of budget constraint: -P(pizza)/P(beer) = -5

D)

New budget constraint: 2B + 5P = 20

New slope: -5/2 = -2.5

New constraint line: See attachment

Answer:

The business must explicitly articulate values that emphasize ethical behavior.

Explanation:

Answer:

450,000 registered voters in the district

Explanation:

Population of interest is defined as the population that is under study and abouth which information is collected. Population of interest can be people, objects, measurements, and so on.

It is from the population of interest that the researcher draws samples that are studied. Insights from studying the sample will be used to draw conclusions about the population.

In this instance 4,000 voters interviewed is the sample. They were drawn from the population of interest made up of 450,000 registered voters in the district.

Where did the answer go after I signed up? I sign up and the answer disapperas?