Answer:

The correct answer is D. All of these.

Explanation:

Mass media are the media received simultaneously by a large audience. Mass communication is the name that receives the interaction between a single broadcaster (or communicator) and a massive receiver (or audience), a large group of people who simultaneously meet three conditions: being large, being heterogeneous and being anonymous. The mass media are only instruments of mass communication and not the communicative act itself.

Federal Communications Commission, because they can stop you from being called from the companies. :)

Answer:

25%.

To start out, general operating expense should not exceed 25%.

Add-on:

i hope this helped at all.

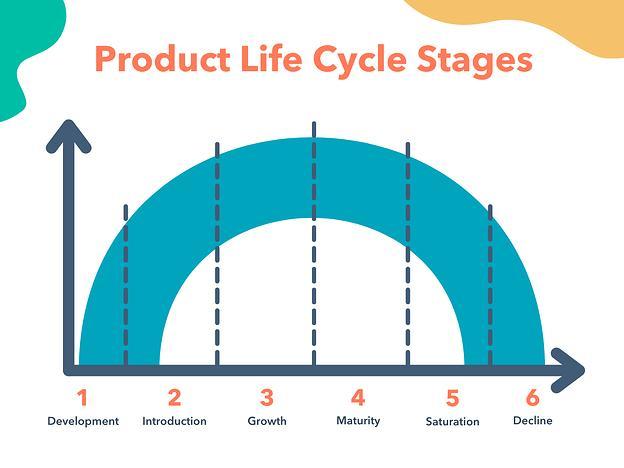

Answer:

Depending on how many stages you like to go by here are the phases

<u>6 Stages:</u>

1. Development

2. Introduction

3. Growth

4. Maturity

5. Saturation

6. Decline

<u>4 Stages:</u>

1. Development/Introduction

2. Growth

3. Maturity

4. Decline

Explanation:

Check the Attached Image!