Answer:

Answer for the question:

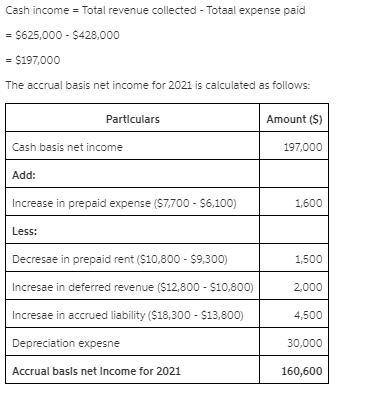

Haskins and Jones, Attorneys-at-Law, maintains its books on a cash basis. During 2021, the law firm collected $610,000 for services rendered to its clients and paid out $425,000 in expenses. You are able to determine the following information about accounts receivable, prepaid expenses, deferred service revenue, and accrued liabilities: January 1, 2021 December 31, 2021 Accounts receivable $ 75,000 $ 67,000 Prepaid insurance 5,800 7,100 Prepaid rent 10,500 9,600 Deferred service revenue 10,500 12,200 Accrued liabilities (for various expenses) 13,500 17,700 In addition, 2021 depreciation expense on office equipment is $28,500. Required: Determine accrual basis net income for 2021.

is given in the attachment.

Explanation:

Answer:

Project Size IRR

A $650,000 14.0%

B 1,050,000 13.5

C 1,000,000 11.2

D 1,200,000 11.0

Explanation:

Based on the information given the set of projects that should be accepted should be the project that has higher Internal rate of return (IRR) than the Weighted average cost of capital (WACC) percentage of 10.8% . Hence, the set of projects that should be accepted are: Project A,B,C,D

Project Size IRR

A $650,000 14.0%

B 1,050,000 13.5

C 1,000,000 11.2

D 1,200,000 11.0

Total $3,900,000

Based on the above we can see that Project A,B,C,D has a total of $3,900,000 which is higher than the retained earnings amount of $2,500,000.

Therefore the set of projects that should be accepted should be Project A,B,C,D

Answer:

$7,732 unfavorable

Explanation:

The computation of the direct labor rate variance is shown below:

Direct labor rate variance = Actual time taken × (Standard rate - actual rate)

= 5,021 labor hours × ($14.71 - $81,591 ÷ 5,021 labor hours)

= 5,021 labor hours × ($14.71 - $16.25)

= $7,732 unfavorable

Since the actual rate is more than the standard rate so it would be lead to unfavorable variance

This is the answer but the same is not provided in the given options

Answer: October 31

Explanation:

It is a 90 day Note so the maturity date will be:

= August 2 + the remaining 29 days in August + 30 days in September + 31 days in October

= October 31

The expiry date will be October 31 as this would be 90 days from August 2, when the note was received.

Answer:

The answer is C. Money Laundering

Explanation:

Solution

From the question stated it can be described as a crime of money laundering.

Money laundering involves the use of illegally obtained money for legitimate purposes.

In this scenario, Jeff uses $15,000 from his illegal sales of drug paraphernalia for setting up a toy store. The origin of the money, which was obtained through illegal method was hidden.

Robbery and larceny are examples of theft that involves stealing items of value from another person. Embezzlement is also a kind of theft. It involves withholding of items with the intention of theft

.