The additional operating cash flow after a new project is called incremental cashflow

The increased operating cash flow that a company obtains as a result of taking on a new project is known as incremental cash flow. If the project is approved, the company will experience an increase in cash flow, which is known as a positive incremental cash flow. A project should receive funding from an organization if the incremental cash flow is positive.

When examining incremental cash flows, it is important to take into account several factors, including the original investment, cash flows from taking on the project, terminal cost or value, and the scope and time of the project. The net cash flow from all cash inflows and outflows during a certain period and between two or more company decisions is known as incremental cash flow.

Learn more about cashflow at

brainly.com/question/24179665

#SPJ4

Answer:

A. $518,000

Explanation:

The computation of the sunk cost is shown below:

= Purchase value of the machine that buys 7 years ago

= $518,000

As sunk cost is the cost that already spent and not relevant for decision making

So according to the given options, the first option is correct

Answer:

Explanation:

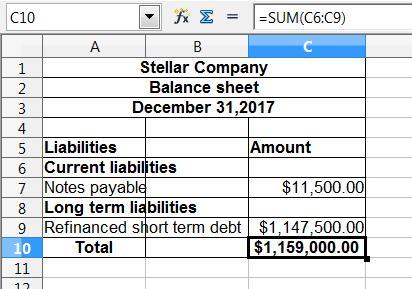

Before showing how short term debt should be presented before doing this we have to classify the items in each head

Like - In current liabilities, notes payable is recorded at $11,500

And, in the long term liabilities, the proceed after brokerage fees for $1,147,500 should be recorded.

The total amount would remain the same i.e $1,159,000

Kindly find the attachment below:

Conducting yourself ethically and legally could have examples of: making products that are trustworthy, don't false advertise (yes, you can legally do things like endorsements and bandwagons, but you can't say "If you buy this product, you will be elected to a high office!".