Answer:

Check the explanation

Explanation:

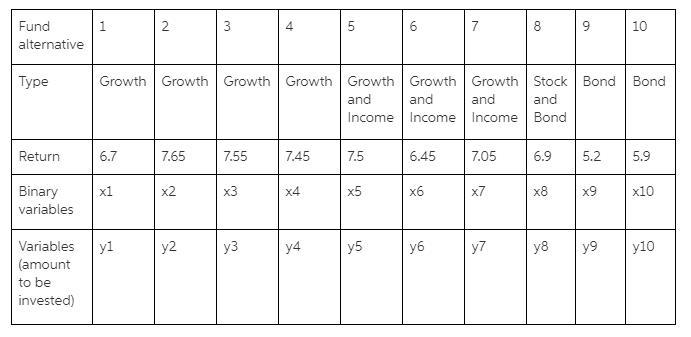

Let the binary variables be: x1,x2,x3.....x10. If x1=0, no amount is invested in fund 1 and if it is 1 it means that an amount is invested. Let y1,y2.....y 10 be the variables for the amount invested.

Kindly check the first attached image for the table.

The objective is to maximize the return. Hence our objective function is: 6.7%*y1+7.65%*y2+7.55%*y3+7.45%*y4+7.5%*y5+6.45%*y6+7.05%*y7+6.9%*y8+5.2%*y9+5.9%*y10. This has to be maximized.

Constraints:

(i) y1,y2.....y10<=25,000 (no more than $25,000 can be invested in any one fund)

(ii) If x1=1, y1>=10,000, 0. This what if formula will be applicable for all the variables. (If a fund is chosen for investment, then at least $10,000 will be invested in it).

(iii) x1+x2+x3+x4<=2 (No more than two of the funds can be pure growth funds)

(iv) y9+y10>=y1+y2+y3+y4 (at least as much as the amount invested in pure amount invested in pure bond funds must be at least as much as the amount invested in pure growth funds)

(v) all x's are binary and all y's>=0. (vi) y1+y2+y3+y4....y10 = 100,000 (amount to be invested)

Solving in excel using the solver function the following solution is obtained:

Kindly check the second attached image for the table.

Thus the maximum return = $7056.25

Amount invested in different funds are:

Kindly check the Third attached image for the table.