Answer:

C) 3.09 years

Explanation:

Calculation for How long has she owned this land

Using financial calculator to calculated the number of years

I/Y = -1.5%

Present value=PV = -$67,900

PMT = 0

Fair value=FV = 64,800

First step is to Press CPT and then N, which will gives us 3.09 years

Therefore has she to owned this land for 3.09 years.

Answer:

A. hold money to transfer purchasing power into the future.

Explanation:

People use money as a store of value when they hold money to transfer purchasing power into the future.

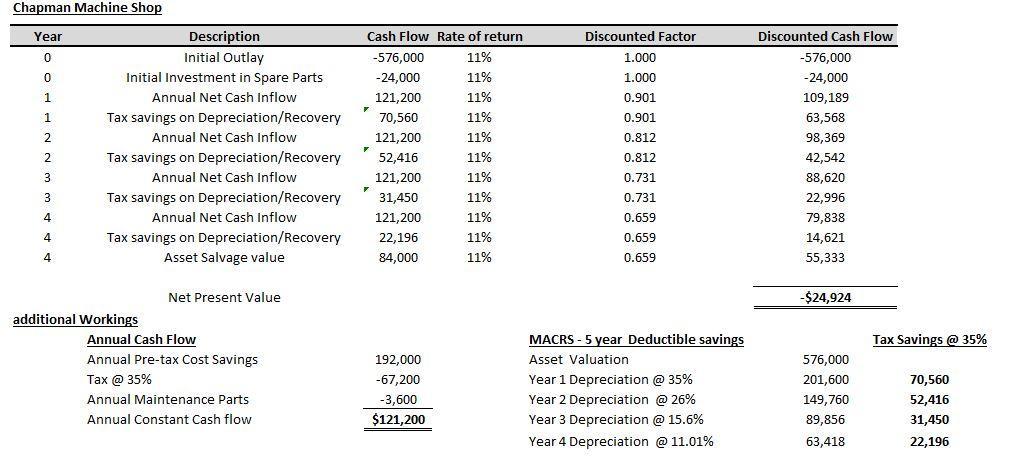

Answer:

The Firm should not Buy and Install the press as it delivers a negative NPV of -$24,924 at 11% discount rate over its 4 year operations

Explanation:

The General rule is to appraise the investment based on various appraisal techniques.

A technique that should be considered must have special focus on the time value of money, the required rate of returns expected by the firm and other Cashflow considerations.

The Net Present Value (NPV) approach will be the best method to proceed with.

The NPV approach typically falls under the following decision tree:

a. If NPV is negative (Reject the proposal)

b. If NPV is positive (Accept if it's a singular project, Accept the highest positive NPV if it's for mutually exclusive Projects)

c. If Zero (this is the breakeven line at which the Project covers all its cost but does not return a profit.) Also referred to as the IRR

Kindly refer to the attached for detailed workings

Answer:

Consider the following explanation.

Explanation:

The international business environment is complex and requires a number of steps to be taken by the organizations that operate in the global environment. The large multinational corporations (MNC’s) should have both strong principles as well as flexible structure to operate at the global level. The strong principles help in creating uniformity at the global level and guide a common organizational culture.

This enables the MNC’s to create a central control over the Global operations and manage the business in an effective manner. On the other hand flexibility is required for adopting the global operations as per the needs of the local conditions. This makes the business responsive and survives in the situations that are not similar to their home country. Thus it can be seen that MNC need to create a balance between strong principles and flexibility. Without either of them it will not be easy for the organization to survive in the complex global business environment.

Answer:$722,000

Explanation:

The over applied overhead of $8000 is deducted from cost of goods sold of $730,000.