Answer:

B. Reduce the Money Market Fund allocation by 30% (to 10%) and put the released funds in AAA-rated corporate bonds

Explanation:

First of all, since the investor is risk averse and cannot afford to lose money on any risky investment, she should change the mix of her investment portfolio but without increasing risks. Corporate bonds that are AAA-rated carry a very low risk and pay a little higher than money market funds. So a small decrease in money market fund assets and an increase in AAA-rated bonds should yield a slightly higher return.

Investing in equities would be too risky and US Treasuries pay even less interests than money market funds.

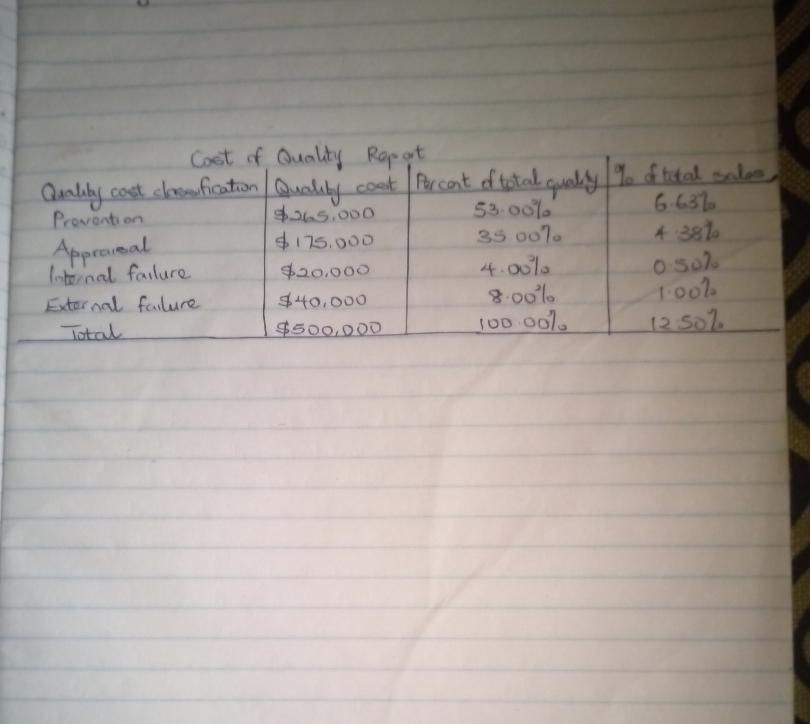

Answer: Check attachment

Explanation:

Quality cost:

Prevention $265000

Appraisal $175000

Internal failure $20000

External failure $40000

Total $500000

Percent of total quality was calculated as:

Quality cost classification/Total

e.g. Prevention = 265000/500000 × 100 = 53.00%

Check attachment for further information.

Answer:

30%

Explanation:

The ratio of free cash flow to sales can be calculated by dividing the free cash flow by the sales amount as follows:

Ratio of free cash flow to sales = $60,000 ÷ $200,000 = 0.30, or 30%.

Therefore, the ratio of free cash flow to sales is 30%.

Answer:

Determination of Gross Profit and Ending Inventory:

a. First-in, First-out (FIFO)

1. Determination of Gross Profit:

Sales $118

Cost of Sales 68

Gross profit $50

2. Determination of Ending Inventory:

Apr. 14 Purchase 1 $73

Apr. 28 Purchase 1 75

Total 2 $148

b. Last-in, First-out (LIFO):

1. Determination of Gross Profit:

Sales $118

Cost of Sales 75

Gross profit $43

2. Determination of Ending Inventory:

Apr. 2 Purchase 1 $68

Apr. 14 Purchase 1 $73

Total 2 $141

c. Weighted average cost methods:

1. Determination of Gross Profit:

Sales = $118

Cost of Sales = 72

Gross profit = $46

2. Determination of Ending Inventory:

Ending inventory = 2 x $72 = $144

Explanation:

FIFO, LIFO, and Weighted Average Cost Methods are different techniques for allocating costs of products to the cost of goods sold and the ending inventory. They produce different results. FIFO assumes that units sold are taken from the units purchased first. LIFO assumes that units sold are taken from the units purchased last. Weighted Average Method uses the average cost to determine the cost to allocate to cost of sales and ending inventory. The average cost is obtained by summing the total inventory costs and dividing it by the units available for sale. Then this average cost is applied to the quantity sold and the quantity remaining to obtain cost of goods sold and value of ending inventory.