Answer:

c. not granting rewards for meeting performance measures

Explanation:

- The incentive compensation refers to the parts pf the employee's salary that is related to the performance and does not guarantee a payment.

- The incentive money includes an additional money or the other rewards of values such as the stock options and that supplements to the base salary.

- These plans act to retain the employees and to identify the shareholders.

Answer:Health statistics

Explanation:

''HEALTH STATISTICS are a vital part of the public health assessment function and are used to identify special risk groups, to detect new health threats, to plan public health programs and evaluate their successes, and to prepare government budgets.''

Health statistics are set of numbers concerning areas of health for example, number of mortality(mortality statistics), birth statistics, marriage statistics and so on.

Health statistics are used to predict the pattern of disease in group of people.

<span>The next action which William would have against Annette for taking the rake is to sue her, blaming her in trespass of personal property. </span><span>A trespass is an </span><span>unauthorized action towards someone's goods. It consists of any contact with the property that was not allowed by the owner, and trespasser, in his turn, is responsible for damage to the property and its owners.</span>

There is more than one reason, but there are two main things they are looking at. They need to see if you are paying on time. The payment history will show if you get behind or not. And because a utility bill is similar to a loan payment, because you have to pay it or you lose your services, they see how responsible you are by checking that. The second major reason they do this is to see what your debt is already. They want to make sure you can afford, with all your bills, to pay them back.

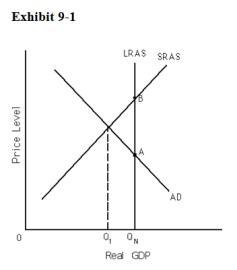

Answer: b) lower in long-run equilibrium than in short-run equilibrium.

Explanation:

A self regulating economy will try to move to the long run Equilibrium.

From the graph attached you will notice that the Price Level at the point where the Long Run Curve intersects with the Aggregate Demand curve is lower than the point where the Short Run Supply curve intersects with the same Aggregate Supply.

This means that Prices in the long term at equilibrium will be less than prices in the short term at Equilibrium should the Economy be a self regulating type that will move towards a long term Equilibrium.