Solution and Explanation:

Step 1: Start Access. Open the downloaded Access file named exploring_a03_Grader_a1.accdb.

Step 2: Assume that there is a table Loans with the following attributes as shown in the screenshot.

Step 3: Create a query using Query Design. From the Clients table, display the client’s FirstName and LastName. From the Accounts table, select the Savings Balance and OpenDate. Sort the query by savings balance in descending order.

Add a calculated field named AccountTime that calculates the number of days each client’s accounts have been open. Assume today’s date is 12/31/2017. Recall dates must be enclosed in # to denote to Access it is a date. Format the results in General Number format. Save the query as Account Longevity, and close the query.

Step 4: Create a query using Query Design. From the Clients table, display the client first name and last name. From the Accounts table, select the savings balance.

Add appropriate grouping, so the client’s total retirement account savings balances are displayed. Add a sort so the highest total savings balances are displayed first.

Step 5: Switch to Datasheet view. Add a totals row displaying the count of the last name and the average of total savings balances. Save the query as Total Balances By Client and close the query.

Step 6: Create a copy of the Total Balances By Client query. Name the query Total Balances By State. Open the query in Design view and remove the client name from the query. Add grouping by the client’s state.

Sort by the client’s state in Ascending order and remove the sort on the savings balance. Add criteria so clients with retirement account savings balances of $10,000 or more are factored in to the query. Save and close the query.

Step 7: Create a new query using Query Design. From the Clients table, select the client first name, last name, and state. From the Accounts table, select the Savings Balance. Add criteria so only customers with balances under $15,000 are displayed.

Step 8: Enter the sample data (one record) as shown in the screenshot.

As present value is given as 25000, loan amount is taken as 25000.

As savings balance is given as 5000, savings balance is taken as 5000.

Step 9: SS

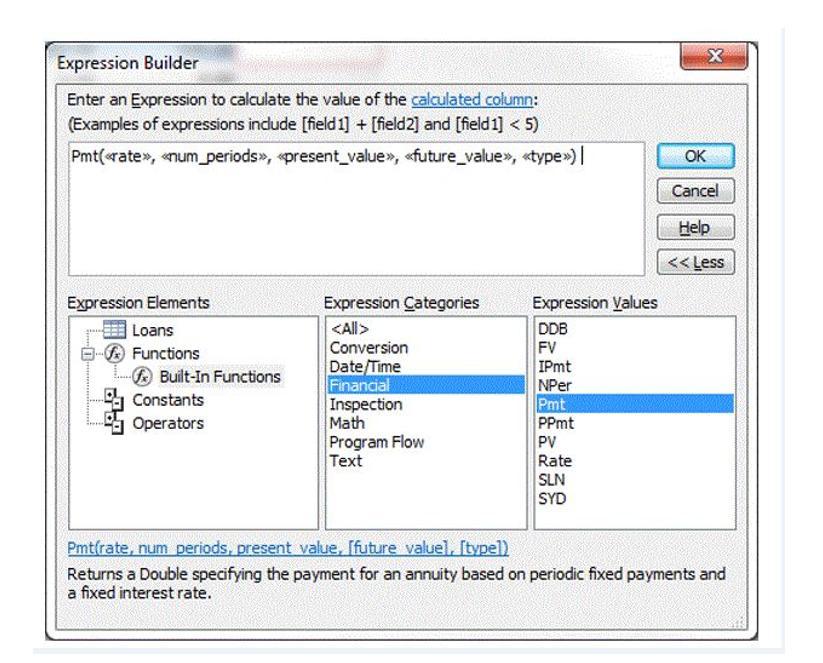

Step 10: Then an expression builder is opened as shown in the screenshot:

Step 11: Then enter the expression pmt(0.5/12, 2*12, - (Loan Amount] – [Savings balance]), 0, 0) as shown in the screenshot.