Answer:

I used an excel spreadsheet to record the accounts using the accounting equation.

What is the ending balance of cash after all transactions have been recorded?

$163,900

Subsequent to shaping a successive approximation to a terminal behavior, I should

use intermittent reinforcement schedule prior to increasing my criteria for reinforcement. An intermittent reinforcement schedule refers to a situation where reinforcement is done after

some behaviors or responses but certainly not after each one.

Answer:

#1 = Web traffic is the amount of data sent and received by visitors to a website. This amount necessarily does not include the traffic generated by bots.

#2 = The three main traffic sources are direct, referral, and search, although your website may also have traffic from campaigns such as banner ads or paid search.

#3 = The time-on-page is simply the time difference between the pageview hit of the next page to the current page. In this scenario, the time-on-page will be “0” seconds since the person did not go to any other page.

#4 = When an employer taxes your bonus using the percentage method, it must identify the bonus as separate from your regular wages. The withholding rate for supplemental wages is 22 percent. That rate will be applied to any supplemental wages like bonuses up to $1 million during the tax year.

#5 = Exit rate as a term used in web site traffic analysis (sometimes confused with bounce rate) is the percentage of visitors to a page on the website from which they exit the website to a different website.

Answer:

Google pays her every time someone clicks on a Google ad on her

site.

Explanation:

Answer:

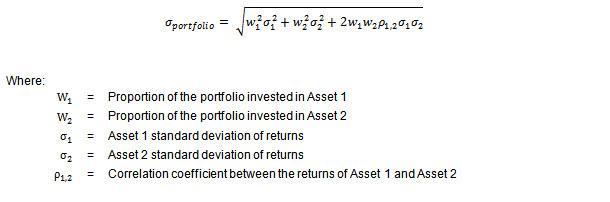

Portfolio Mean = 7.2%

Portfolio Stdev = 0.1169615 or 11.69615% rounded off to 11.70%

Explanation:

The mean return of a portfolio consisting of two securities can be calculated by multiplying the weight of each security in the portfolio by the mean return of that security and adding the products for each security. The formula for two asset or security portfolio return (mean) can be written as follows,

Portfolio Mean = wA * rA + wB * rB

Where,

- w represents the weight of each security

- r represents the mean return of each security

Portfolio Mean = 60% * 8% + 40% * 6%

Portfolio Mean = 7.2%

The standard deviation is a measure of the total risk. The standard deviation of a portfolio consisting of two securities can be calculated using the attached formula.

Portfolio Stdev = √(0.6)² (0.2)² + (0.4)² (0.15)² + 2(0.6) (0.4) (-0.3) (0.2) (0.15)

Portfolio Stdev = 0.1169615 or 11.69615% rounded off to 11.70%