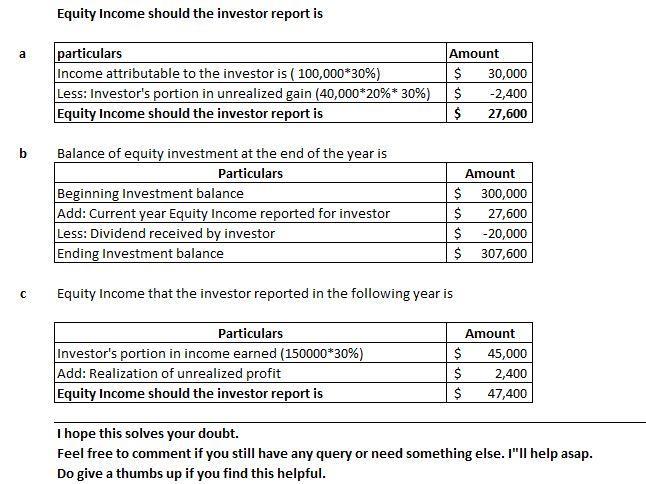

Assume that an investor owns 30% of an investee, and accounts for its investment using the equity method. At the beginning of the year, the Equity Investment was reported on the investor's balance sheet at $300,000. During the year, the investee reported net income of $114,000 and paid dividends of $20,000 to the investor. In addition, the investor sold inventory to the investee, realizing a gross profit of $48,000 on the sale. At the end of the year, 20% of the inventory remained unsold by the investee.

Answer:

d. Design utilization is 66%.

Explanation:

If the clinic gave flu shots to 330 seniors over ten hours, that's an average of 33 seniors per hour, comparing to the design capacity and effective capicity gives:

Therefore, Design utilization is 66% and Effective utilization is 75% so the answer is D.

Answer:

6,000 units

Explanation:

We know that

Break even point in units = (Fixed expenses ) ÷ (Contribution margin per unit)

where,

Contribution margin per unit = Selling price per unit - Variable expense per unit

The selling price would be

= $500 - $500 × 4%

= $500 - $20

= $480

And, the Variable expense per unit is $350

So, the contribution margin per unit would be

= $480 - $350

= $130

So, the break even point in unit should be

= $780,000 ÷ $130 per units

= 6,000 units

Answer:

<u>Interlocking corporate director</u>

Explanation:

Interlocking corporate director refers to an individual serving as a director on the board of multiple companies.

Interlocking directorship is not considered illegal if the companies of which the same individual serves as a director, are not competing firms.

In the given case, an individual serves on the board of a bank, also serves the board of a computer manufacturing company that usually borrows from the bank.

Here, the independence and objectivity of the director would be impaired and this may lead to a situation of conflict of interests as the director exercises sizable influence in framing the lending policies of the bank.

Thus, such a situation would be in violation and the director may have to step down from the board of one of the companies.

To review and report on internal controls over sales, purchasing and cash at Downe, your external audit firm should develop points for inclusion in your firm's report on identified internal control deficiencies at Downe.

In the cases described, the central deficiency is in the use of money not specifically allocated for payments and lack of adherence to company policy.

The consequences of these actions at Downe can mean a lack of control, organization and coordination of the flow of income and expenses, leaving businesses without correct records of capital utilization, legal compliance and inventory control.

It will therefore be necessary to restructure Downe's processes in order to implement a new policy that is passed on to all employees to be strictly enforced. In addition to greater control by managers and redesign of the organizational and work structure.

In this way, the company will guarantee that the processes occur in a planned, focused and strategic way, generating an improvement in the organizational culture and better positioning for the company in the market.

Find out more information about external auditor here:

brainly.com/question/25388600