<span>Carl Jung's view of the extroverted and introverted types serves as the basis of the Myers-Briggs Type Indicator. This is a personality questionnaire that gives a type to a person based on social, organizational, thinking patterns, and other personality indicators.</span>

Investing is when you invest or expend your money into a business, stock, etc to make money. You can always invest safely or be risky but have a chance of losing your money. Saving is when you save up you money and don’t do anything with it neither spend it or invest it.

Answer:

Acknowledge his/her understanding of criminal sanctions for unauthorized use 20

Explanation:

According to the Department of Highway Safety and Motor Vehicles Division of Motorist Services DRIVER AND VEHICLE INFORMATION DATABASE otherwise known as DAVID.

In order to comply with DAVID Memorandum of Understanding requirements, a user must acknowledge understanding of criminal sanctions for unauthorized use 20.

Also, a user must acknowledge his/her understanding of the confidentiality of information

The answer that is being described above is the broad emphasis. This are used by other artists in which they used this method when they try to pin point about something and tries to express them in their artwork without any exact rule or part to place the artwork that is being done. It is mostly used to point out the entire artwork that the artist is trying top point out or give the message.

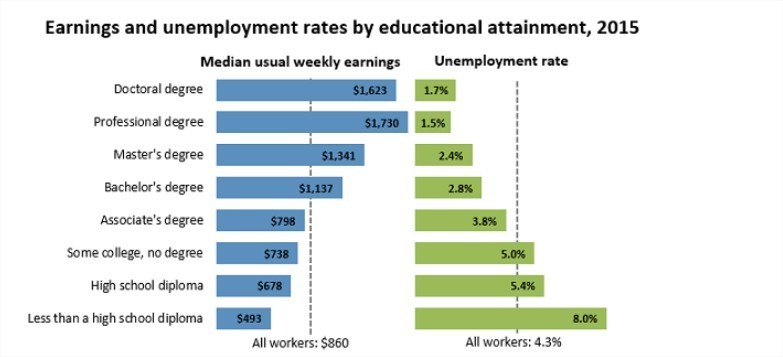

<span>According to the U.S. Department of Labor Statistics, in 2009 high school graduates made approximately $ 32,544/Year, <span>whereas</span>,</span><span> those who did not complete high school </span>made approximately $23,664.

Which mean the ones who graduated the high school earned around

$10,000 more than the ones without a high school degree.