Answer:

Ping Pong Ltd

i. No. The bank has not breached its duty of care to its customer, Ping Pong Ltd.

ii. No. The customer, Ping Pong, has not breached its duty of care to its bank.

Explanation:

The breach occurred between Mr. Z. and Ping Pong. Certainly, Mr. Z. breached his professional and fiduciary duty of care to Ping Pong, his employer. By presenting forged documents as evidence of supply transactions, Mr. Z. has fraudulently defrauded his employer to the tune of $6.6 million. It is the responsibility of Ping Pong to recover from Mr. Z. as soon as the fraud is discovered.

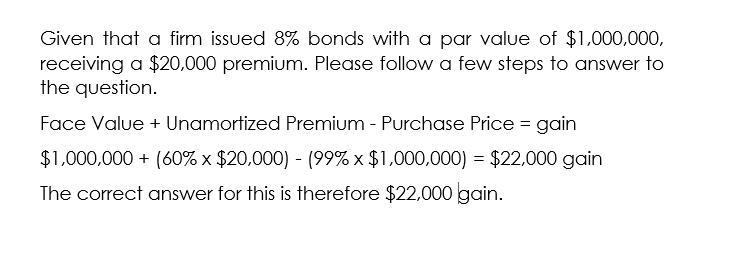

Answer:

$63.01

Explanation:

The share price today is the present value of expected future cash flows which in this case are the expected future dividends and the terminal value of dividends beyond the 3rd year.

Year 1 dividend =$2.2

Year 2 dividend =$3.9

Year 3 dividend =$4.8

Terminal value=Year 3 dividend*(1+constant growth rate)/(required rate of return-constant growth rate)

constant growth rate=2%

the required rate of return=9%

Terminal value=$4.80*(1+2%)/(9%-2%)

Terminal value=$69.94

Present value of a future cash flow=cash flow/(1+required rate of return)^n

n is 1 for year 1 dividend, 2 for year 2 dividend , 3 for year 3 dividend, and terminal value(terminal value is stated in year 3 terms)

stock price=$2.2/(1+9%)^1+$3.9/(1+9%)^2+$4.8/(1+9%)^3+$69.94/(1+9%)^3

stock price=$63.01

Answer:

economics a situation in which the market demand for a commodity is greater than its market supply, thus causing its market price to rise.

Explanation:

this is the definition. hope this helps.

Answer:

b. the implied warranty of merchantability

Explanation:

Implied warranty of merchantability refers to an implied assurance, in every sales transaction that the seller's goods are safe and fit for intended purpose of usage.

It represents an unspoken guarantee on the part of the seller that his goods conform to the acceptable standards and properly packaged and labeled and abide by the promises conveyed on their label.

The motive behind such a warranty being, the seller must properly inspect and test the quality of his goods before releasing them or making them available for sale in the market.

In the given case, the seller sold skis to the customer which cracked into two upon usage. The seller isn't aware of the cause of the consequence. Thus, the seller breached the principle of implied warranty of merchantabilty as per which, it should've first checked and inspected the skis before making them available for sale.