Answer:

1986 is the base year. so, the CPI of the base year is always 100%.

Option A

The value of $100 in 1993 would be = ($100/CPI of 1986) * CPI of 1993

= ($100/100) * 135

= $135

So, Option A is true.

Option B

$100 in 1992 would have been worth in 1986: ($100/CPI of 1992) * CPI of 1986

= ($100/120) * 100

= $83.33

So, Option B is false.

Option C

$100 in 1991 would have been worth in 1986: ($100/CPI of 1991) * CPI of 1986

= ($100/110) * 100

= $90.91

So, Option C is false.

Option D

The value of $100 in 1992 would be: ($100/CPI of 1993) * CPI of 1992

= ($100/135 * 120

= $88.89

So, Option D is false.

Answer:

18.18%

Explanation:

Income = Coupon amount over the period of holding

Income =($1000*8%)*5

Income =$400

Capital gain/(loss)=Sale price - Purchase price

Capital gain/(loss)=$900 - $1100

Capital gain/(loss)=-$200

Total percentage return=[(Income+Capital gain)/Purchase Price]*100

=[$400+(-$200)]/$1100]*100

=[$200/$1100]*100

=18.18%

<u>Answer:</u>

<em>(d) Perishability is the reason for Eat and Den's loss of revenue</em>

<em></em>

<u>Explanation:</u>

Perishability is utilized in marketing to show how capacity service cannot be put away available to be purchased later on. It is a fundamental idea of service showcasing.

One of the urgent variables/issues looked by advertisers is the perishability factor in services showcasing. Administrations have Zero Inventory! When sold, they stand sold and can't be returned. Subsequently, a few times in the administration's business, the maxim "Early introduction is the last impression" really holds genuine. Similarly, in Eat and Den, the eatable goods are all perishable and cannot be reused the next day hence the restaurant incurs significant loss.

Balance transfer fee is NOT a common credit card fee.....

HOPE it helps!!!!

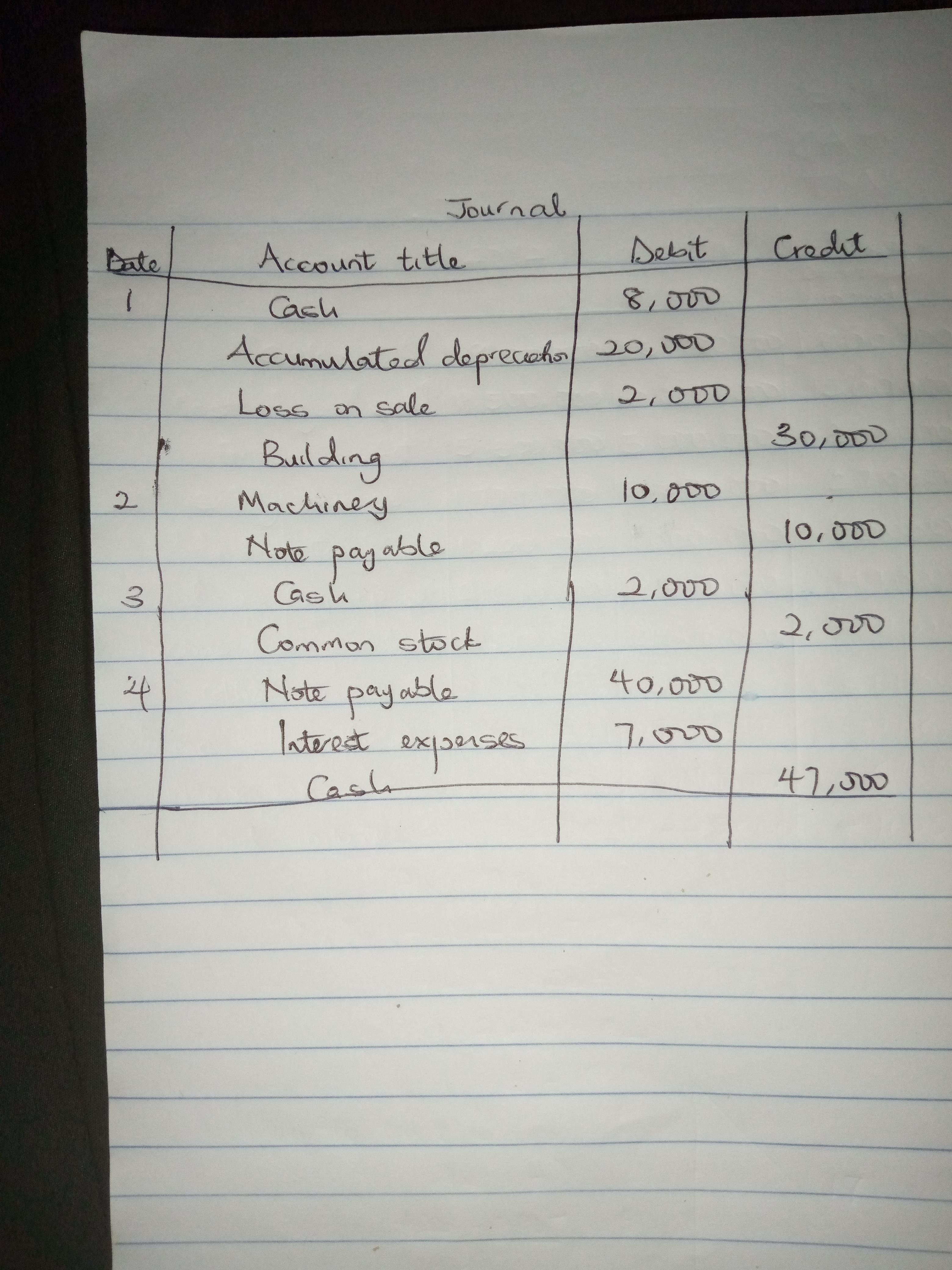

Answer: The answer is provided below

Explanation:

a. The reconstructed journal entry has been prepared and attached.

b. The following are the effects it has on the investing section or the financing section of the statement of cash flows.

The first transaction will lead to a cash inflow of $8,000 from the investing activities.

The second transaction is non-cash transaction therefore, it will not be reported in either the financing or the investing activities.

The third transaction will lead to a cash inflow of $2,000 from the financing activities.

The fourth transaction will lead to a cash outflow from the financing activities.

Thw diagram has been attached.