Juan needs to spend $3 from his pocket to start the lemonade stand to earn money.

To start the lemonade stand, Juan needs to purchase materials before selling his product and earning money. For this he needs money. His mother agreed to give him $10 as a loan to start a lemonade stand. To purchase the required item, he made a list of items to buy:

Add all the supply item prices to know how much money he required.

So

Price of cups + price of Lemon + Price of sugar

=$2 + $8 + $3 = $13.

He needs $13 to start the lemonade stand.

But his mother give him $10 as a loan, now the required money is

$13-$10=$3.

Juan needs to invest $3 from his pocket to start the lemonade stand and earn money.

You can learn more about earn money from lemondae at

brainly.com/question/1301117

#SPJ4

Answer:

33.33%

Explanation:

Let weight of T-bill be x, therefore weight of stock will be 1-x

Portfolio = Weight of stock*Beta of stock + Weight of T-bills*Beta of T-bills

1 = (1-x)*1.5 + x*0

1 = 1.5 - 1.5x

x = 0.5/1.5

x = 0.3333

x = 33.33%

Therefore, the percentage of the portfolio invested in treasury bills is 33.33%.

Answer:

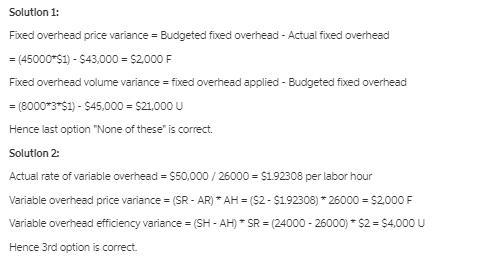

1. U. None of these

2. Variable overhead price variance = $2,000 F

Variable overhead efficiency variance = $4,000 U

Explanation:

Please see attachment.

Answer:

The correct answer is letter "C": paid out of aftertax profits.

Explanation:

A dividend is a cash distribution by a company to its shareholders. It is a payment made as a bonus to investors from publicly listed firms or funds for putting their money into the project. They can be paid either in cash or in stocks or sometimes in other forms of property only when the aftertax earnings have been calculated.