Answer:

Step-by-step explanation:

hello,

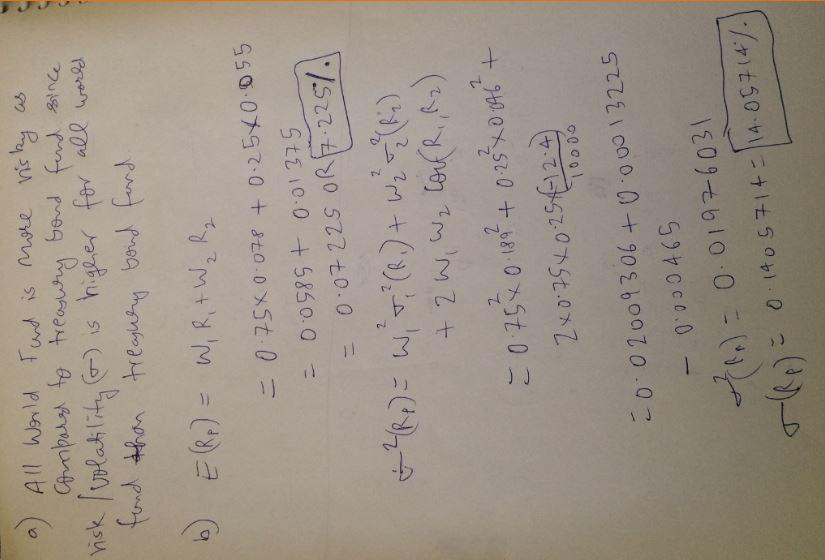

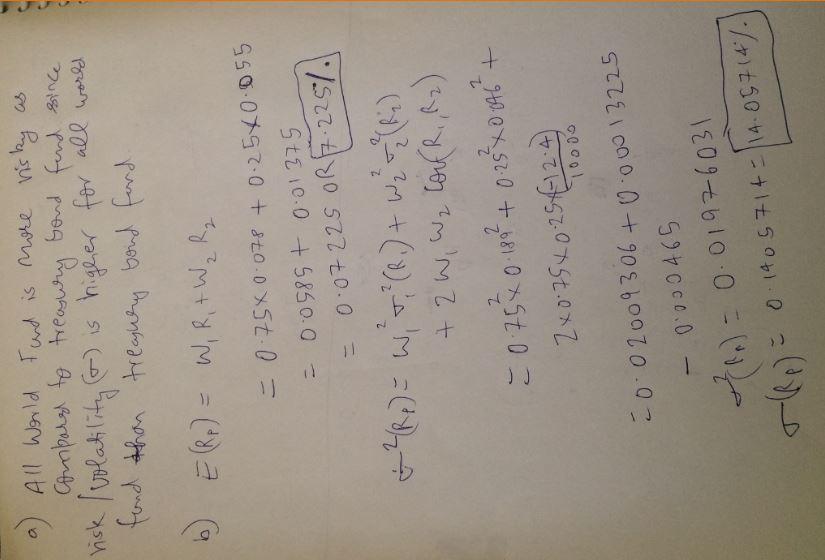

we will denote the expected return of investment in the all world fund as E(A).

we will also denote the standard deviation of investment in the world fund as S(A).

we will denote the expected return of investment in the treasury bond fund as E(T)

we will also denote the standard deviation of investment in the treasury bond fund as S(A).

A. since S(A) = 18.90% and S(T) = 4.60%. We see that the standard deviation for all world is greater than that of treasury fund, thus the fluctuation in all world fund is higher than that of treasury fund, hence the all world fund is more risky.

B. expected percent return of portfolio = (percentage investment in the all world × E(A) ) + (percentage investment in the treasury fund × E(T) )

=( 75% × 7.80%) + ( 25% × 5.5%)

= 7.225%

standard deviation percent of portfolio = (percentage investment in the all world × S(A) ) + (percentage investment in the treasury fund × S(T) )

= (75% × 18.90%) + ( 25% × 4.60%)

= 15.325%

expected return in dollars for a client investing $10,000

= 7.225% × $10,000

= $722.500

standard deviation return in dollars for a client investing $10,000

= 15.325% × $10,000

= $1,532.500

C. similarly, we simply follow the same procedure in (b) above.

expected percent return of portfolio = ( 25% × 7.80%) + ( 75% × 5.5%)

= 6.075%

standard deviation percent of portfolio = (25% × 18.90%) + ( 75% × 4.60%)

= 8.175%

expected return in dollars for a client investing $10,000

= 6.075% × $10,000

= $607.5

standard deviation return in dollars for a client investing $10,000

= 8.175% × $10,000

= $817.5

D. i will recommend portfolio (b) for an aggressive investor because it more risky since its standard deviation is $1,532.500 and it generates more expected return of $722.500 but i will advice a conservative investor to go for portfolio (c) because it is less risky since its standard deviation is $817.5