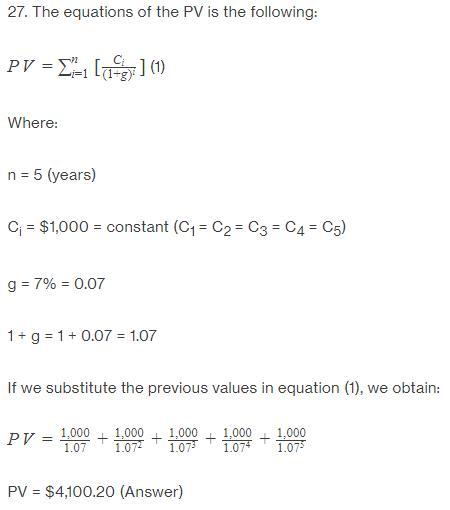

Answer:

The annuity is worth $4100.20 today and if we increase the rate of return, from 7% to 8% the value of the annuity falls to $3992.71.

Explanation:

The step by step solution for the given problem is attached with the image.

The value of annuity will decrease if we increase the rate of return, from 7% to 8%. Future cash flows are discounted using the rate of return, and the higher the discount rate, the lower the present value of the future cash flows.

Answer:

15.7

Explanation:

In this question we have the following information

Employment in Motor Vehicle manufacturing within city = 12643

Total employment in motor city = 560379

Total individual employment = 152750

Total employment = 106201232

We get the location quotient as

(12643/560379)/152750/106201232

0.02256/0.001438

= 15.69

This is approximately

15.7

Therefore the location quotient = 15.7

Answer: Option B

Explanation: In simple words, lean manufacturing refers to the manufacturing process in which the production firm focuses on minimizing the waste that occurs in the production process and also increases the productivity at the same time.

This system was first implemented in Japanese manufacturing industry and lead to decrease in cost of production significantly. Such kinds of manufacturing is highly evident in industries prancing goods such as clothes, shoes etc.

This strategy also decreases the production cycles and increase the respond time of the firm to the market.

Answer:

It is logical to use this method when overhead resources are consumed by various products in substantially different ways throughout multiple departments.

Explanation:

A departmental overhead rate is considered to be a standard charge based on the units of activity produced by a business segment. Overhead rate at the department level are usually applied in a more refined cost allocation environment, where there is a need to apply overhead cost as precisely as possible.

Answer:

C)capitalist

Explanation:

Market economies and mixed economies can be described as capitalist economies. In capitalist economies, private individuals and firms own the factors of production or capital goods. The private sector produces goods and services consumed in the economy. The motive for producing the goods is the private sector's self-interest or profits.

The free enterprise market is the purest form of a capitalist economy. Capitalist economies contrast with socialists economies where ownership of capital goods is in the government's hands.