Answer:

B. Although you can hire someone to keep your books, you'll still need to know how to read, understand, and interpret basic accounting reports in order to make good business decisions

Explanation:

You may employ someone to manage the accounts, but you do need to know how to read, understand, and interpret simple reports of accounting to make sound business decisions, as well as understanding whether someone is committing fraud with you. A simple knowledge can help with all of this.

The smooth operation of a company is practically impossible without being able to interpret, comprehend and evaluate accounting reports and financial statements.

Therefore according to the given situation, the correct answer is b

Executive compensation includes benefits such as salaries, perks, incentives, and insurance.

It's hard to read business news without encountering articles about salaries, bonuses, and stock option packages given to CEOs of publicly traded companies. It's not easy to understand the numbers for evaluating how companies are paying their top talent. Investors must ensure that executive compensation works in their favor.

The board, at least in principle, seeks to align management's actions with the company's success through remuneration agreements. The idea is that the CEO's performance adds value to the organization. “Pay for performance” is the mantra most companies use when describing compensation plans.

Most people can support the idea of paying for results, but this concept implies that the CEO takes risks. The CEO's wealth should scale with the company's wealth. When considering a company's compensation program, look at the extent to which management is involved in generating returns for investors.

Learn more about Executive Compensation here : brainly.com/question/14391055

#SPJ4

Answer:

True

Explanation:

A more precise way to describe the situation is that Joe's pizza parlor is a monopolistic competition. But that definition considers that all 'food' items have some degree of close substitute relation.

But yes, if you consider this two conditions:

- a broad definition of monopoly

- other restaurants are not considered close substitutes for the food sold at the pizza parlor

Then yes, Joe has monopoly

The correct answer is False

Explanation:

Child care providers are usually professionally prepared individuals who take care of children, this includes teachers, babysitters, nannies, counselors, etc. Additionally, child care providers can work in specific institutions such as schools or take care and supervise children in the child's home. In most cases, being a child care provider implies dealing with different children and therefore different personalities, needs, and conditions.

Due to this, it is common child care provides find themselves caring for a child with conditions such as measles, food allergies, bronchitis, and even asthma. In the case of asthma, this is can be found in around 10% of children, and therefore it is not extremely uncommon child care providers had to take care of a child with asthma.

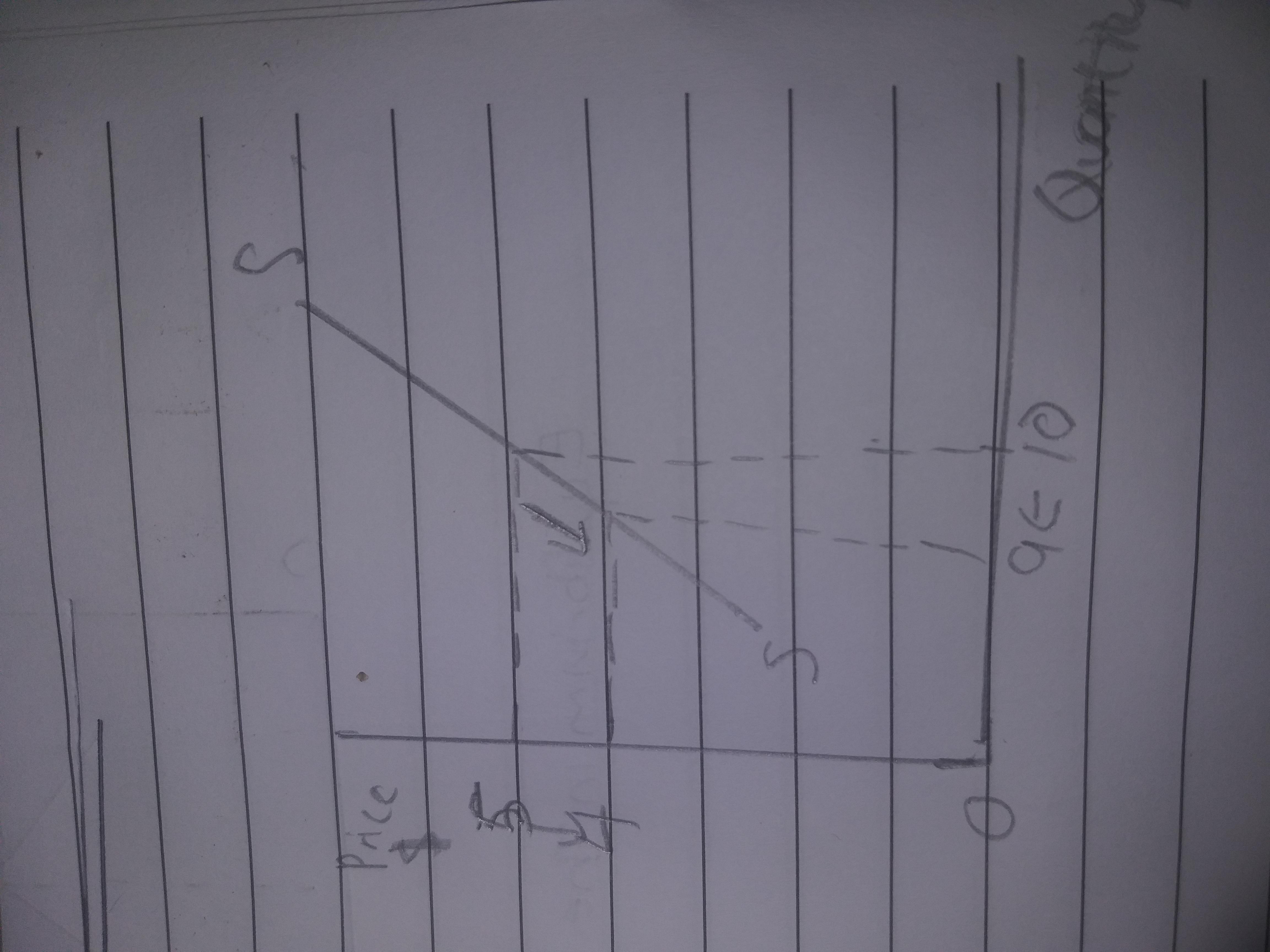

Answer:

A. a movement downward along the supply curve.

Explanation:

According to the law of supply, the higher the price, the higher the quantity supplied and the lower the price, the lower the quantity supplied.

This accounts for why the supply curve is positively sloped.

A change in price of a good leads to a movement along the supply curve and not a shift of the supply curve.

Please check the attached image for a graph showing the supply curve