Answer:

Word of Mouth.

Explanation:

As Magnira Inc. is trying to promote its cosmetics. It offers discounts to customers who post about its products' benefits in their social media accounts. This enables others to know about the company's products. In this case, customers of Magnira Inc. are involved in word of mouth. Word of mouth is considered as more authentic, valid and reliable source of information for the customers. Customers truly believe that its more genuine kind of information which is coming from the customers not the company itself, therefore, customer pay more attention to it and give more weightage to it. Customers do not believe much on the advertisement because they know that ads are being aired by the company itself and it is the paid from but word of mouth are the true and genuine comments and feedback of the customers who have used the brand by themselves.

Answer:

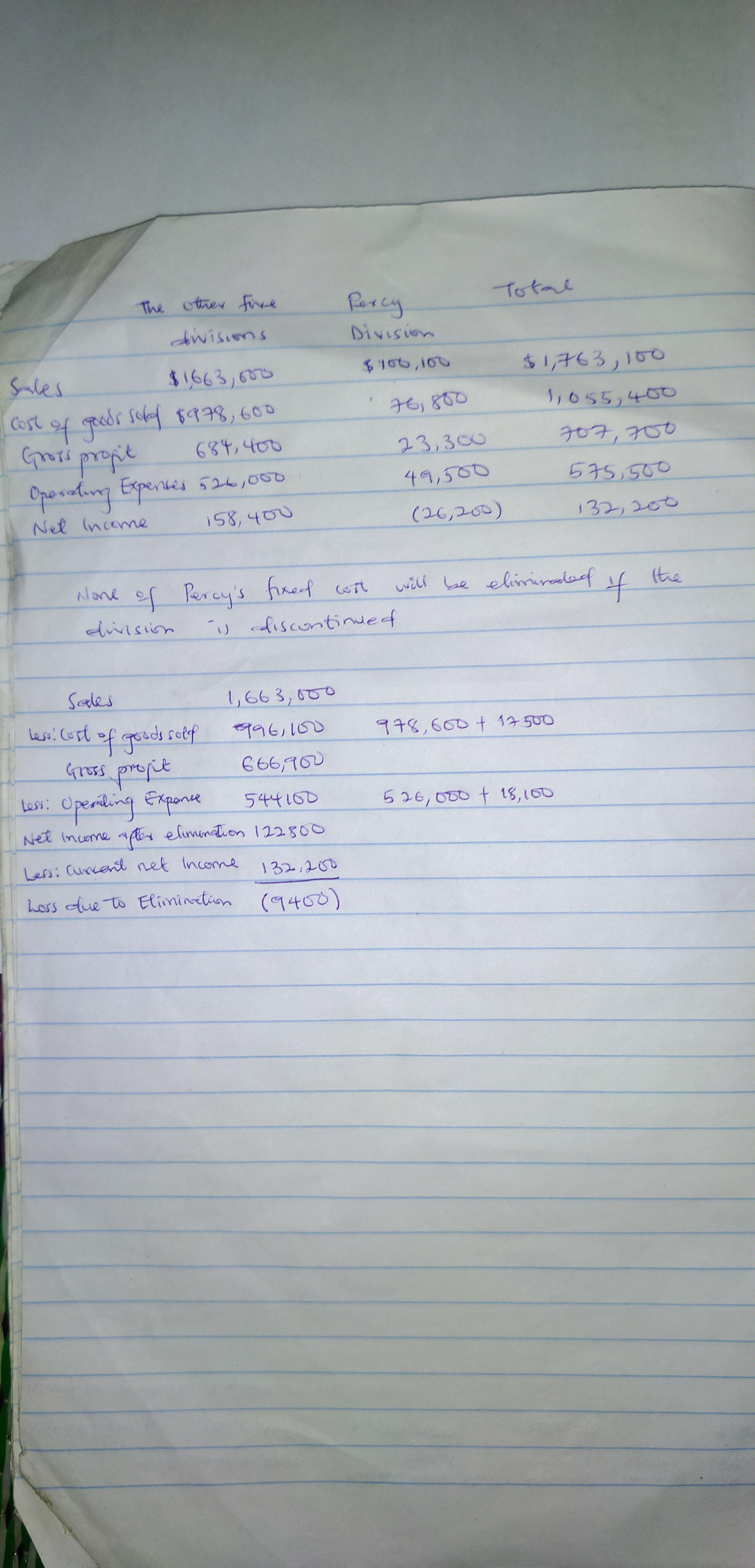

Veronica is wrong because if Percy division is close, it's fixed won't be eliminated and as such the cost will be shouldered by the other divisions which will lead to a $9,400 reduction in profit.

Though eliminating Percy division will prevent the loss of $26,200. However with a fixed cost totalling $35600 which will have to be beared by other five divisions, eliminating Percy division won't be a good idea.

Explanation:

Kindly chech attached picture

Answer:

$25,000

Explanation:

Calculation to determine How much goodwill should be recognized by Rommer Company when recording the purchase of Daley Inc.

Using this formula

Goodwill=Beginning cash-Ending book value-Fair value tangible assets-Fair value intangible assets

Let plug in the formula

Goodwill=$4,700,000-$4,000,000-$525,000-$150,000

Goodwill=$25,000

Therefore the goodwill that the company should be recognized by Rommer Company when recording the purchase of Daley Inc. $25,000

One positive effect: Technology has improved areas in medicine, and therefore has generally allowed humans to have a longer life span.

One negative effect: Over usage of technology (i.e. phones) can disrupt sleeping habits and lead to sleep disorders.

Answer:

The correct answer is A. increase tax rates and/or reduce government spending.

Explanation:

Increasing the tax burden is an easy way for the state to increase its income temporarily and subject matter, but it turns out that increasing the tax burden affects productivity and consumption, so in the end the income of the productive sector is diminished, and more taxes on a lower taxable base does not imply increasing revenues.

When a government decides to reduce public spending for a fiscal balance, it is limited to reducing the social assistance and social security, but not to reduce the bureaucratic apparatus that curiously is usually high in countries with economic crisis, and also Be a source of corruption corruption.