Around <span>+$2 billion. would be the answer!</span>

Since the company is following a periodic inventory system, it has to use temporary accounts to record sales and purchases.

Transaction A

Purchases – Dr 860500

Accounts payable 860500

Transaction B

Accounts payable - Dr $111,600

Purchase returns $111,600

Transaction C

Accounts payable - Dr 748900

Discount received 14,978

Cash 733,922

Answer:

Option D. None of the other options fit.

Answer:

The answer is: the following three should be used.

- net present value (NPV)

- traditional payback period (PB)

- the modified internal rate of return (MIRR)

Explanation:

First of all, the NPV of the four projects must be positive. Only NPV positive projects should be financed. If the NPV is negative, the project should be tossed away. This is like a golden rule in investment.

Now comes the "if" part. What does the company value more, a short payback period or a higher rate of return.

If the company values more a shorter payback period (usually high tech companies do this due to obsolescence), then they should choose the project with the shortest payback period.

If the company isn't that concerned about payback periods, then it should choose to finance the project with the highest modified rate of return. This means that the most profitable project should be financed.

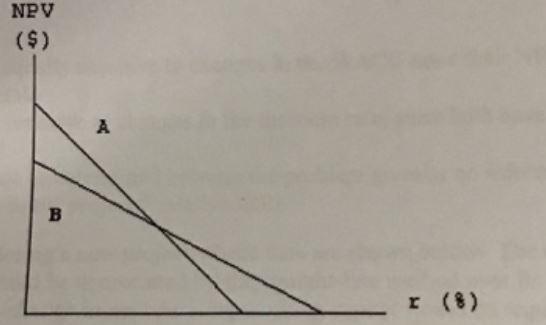

Answer: a. More of Project A's cash flows occur in the later years.

Explanation:

When a project has its cashflows occurring in later years, the NPV will be less because the discount rate would have a greater period to discount it in as opposed to cashflows that occur more recently which would receive less discounting from the discount rate.

As a result of Project A having more distant cashflows, the discount rate discounted its cash flows more which is why higher rates led to its NPV being zero because those higher rates got to discount it over a longer period.