hola**co'mo esta'sdssfsrfetryrtpoqqll

Answer:

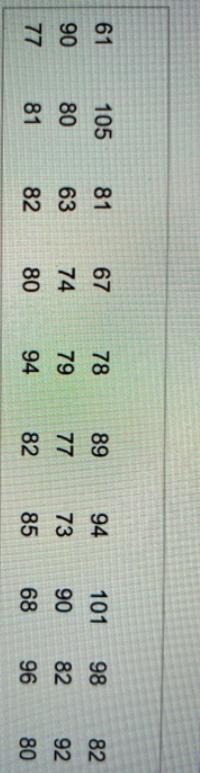

23.33%

Step-by-step explanation:

The computation of the percentage of days in a month for running out of cash is shown below:

Percentage of running out of Cash is

= (Relevant Occurrence of an event ÷ Total number of events) × 100%

where,

The Relevant occurrence of an event is 7 (105,94,101,98,94,96,92)

And, the total number of events is 30 i.e. 30 days

So, the percentage is

= 7 ÷ 30 × 100

= 23.33%

Answer:

(0,6)

(1,5)

(2,4)

(3,3)

(4,2)

Step-by-step explanation:

To solve this table first convert the equation to slope-intercept form (y=mx+b), to do this solve for y in the equation. The slope-intercept form is y=-x+6, where -1 is the slope and 6 is the y-intercept. Then from that, you can get your first point, because you know the y-intercept is 6, therefore when x equals 0 y must be 6. Next, because the slope is -1 that means the y-value decreases by 1 every time the x-value increases by 1. So to find the rest of the y-values simply subtract 1 from the previous y-value.

There are 6.4 Kilometers in 4 miles

X=first number

y=second number

x=y+5

3x+2y=30

3(y+5)+2y=30

3y+15+2y=30

5y+15=30

5y=30-15

5y=15

y=3

x=3+5

x=8