Answer:

$489,512.15

Explanation:

The formula for calculating future value:

FV = P (1 + r)^n

FV = Future value

P = Present value

R = interest rate

N = number of years

We are supposed to determine the present value

Present value is the sum of discounted cash flows

Present value can be calculated using a financial calculator

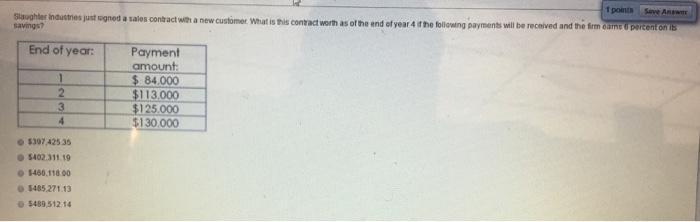

Cash flow in year 1 = 84,000

Cash flow in year 2 = 113,000

Cash flow in year 3 = 125,000

Cash flow in year 4 = 130,000

I = 6%

PV = 387,739.47

387,739.47(1.06)^4 = $489,512.15

To find the PV using a financial calculator:

1. Input the cash flow values by pressing the CF button. After inputting the value, press enter and the arrow facing a downward direction.

2. after inputting all the cash flows, press the NPV button, input the value for I, press enter and the arrow facing a downward direction.

3. Press compute