<span>True. Parks and natural areas provide an avenue for humans to conduct adventure programs and activities. with proper stewardship and preservation, parks and natural areas provide a conducive place for outdoor recreation and education programs that may lead to increased health, wellness, and community participation.</span>

Answer:

The correct answer is the option E: consumers are encouraged to buy domestically produced goods.

Explanation:

To begin with, in order to the economy to grow the country must encourage the consumers to buy more domestically produced goods so that the when the demand increases so does that income of the firms and that impacts in the demand that the companies do as well. Therefore that the country, and that is, the firms and the government, should encourage the increase of consumption from the buyers in order to intend to experience an economic growth.

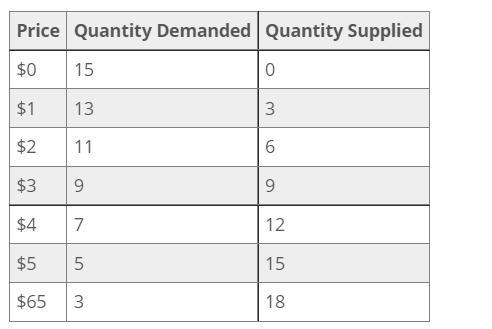

Answer:

$3

Explanation:

A price floor is when the government or an agency of the government sets the minimum price of a product. A price floor is binding if it is set above equilibrium price.

Price ceiling is when the government or an agency of the government sets the maximum price for a product. It is binding when it is set below equilibrium price.

Equilibrium price is the price at which quantity demand equal quantity supplied. Above equilibrium price there is a surplus - quantity supplied exceeds quantity demanded.

Below equilibrium price there is a shortage - quantity demanded exceeds quantity supplied

Shortage = $12 - $9 = $3

Answer:

The correct answer is d. liquid financial assets that for tax purposes must be reinvested in the firm if not distributed as dividends to shareholders.

Explanation:

One of the variables that best measure a company's financial capacity is free cash flow (FCF). It consists of the amount of money available to cover debt or distribute dividends, once payment to suppliers and purchases of fixed assets (construction, machinery ...) have been deducted.

In general, this calculation serves to measure the ability of a business to generate cash regardless of its financial structure. That is, the FCF is the cash flow generated by the company that is available to meet payments to its financing providers.

In short, the FCF is the balance of treasury that is free in the company, that is, the money available once the mandatory payments have been met. Normally, the FCF is used to remunerate shareholders via dividends or to amortize the principal of the debt and meet interest.