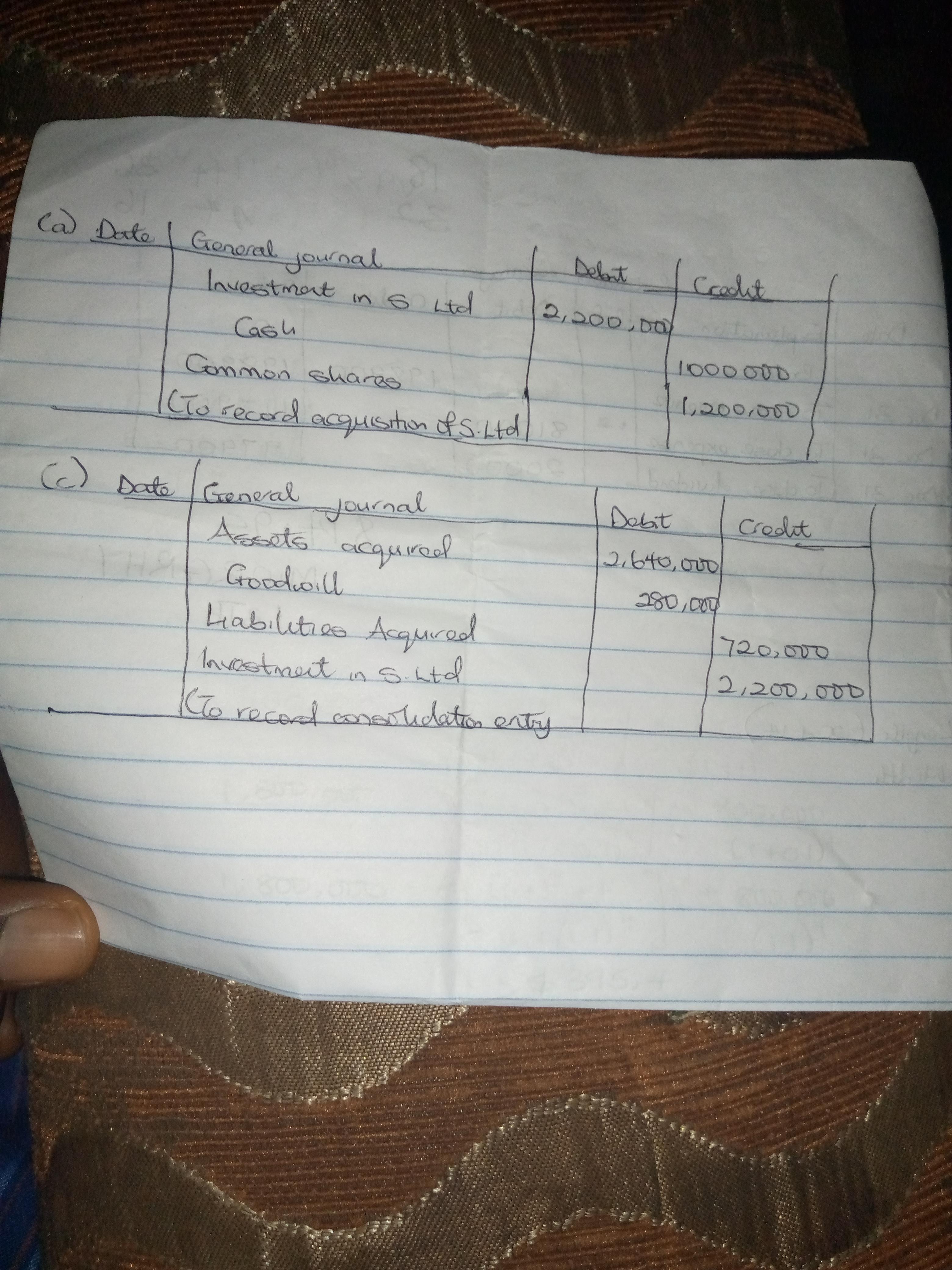

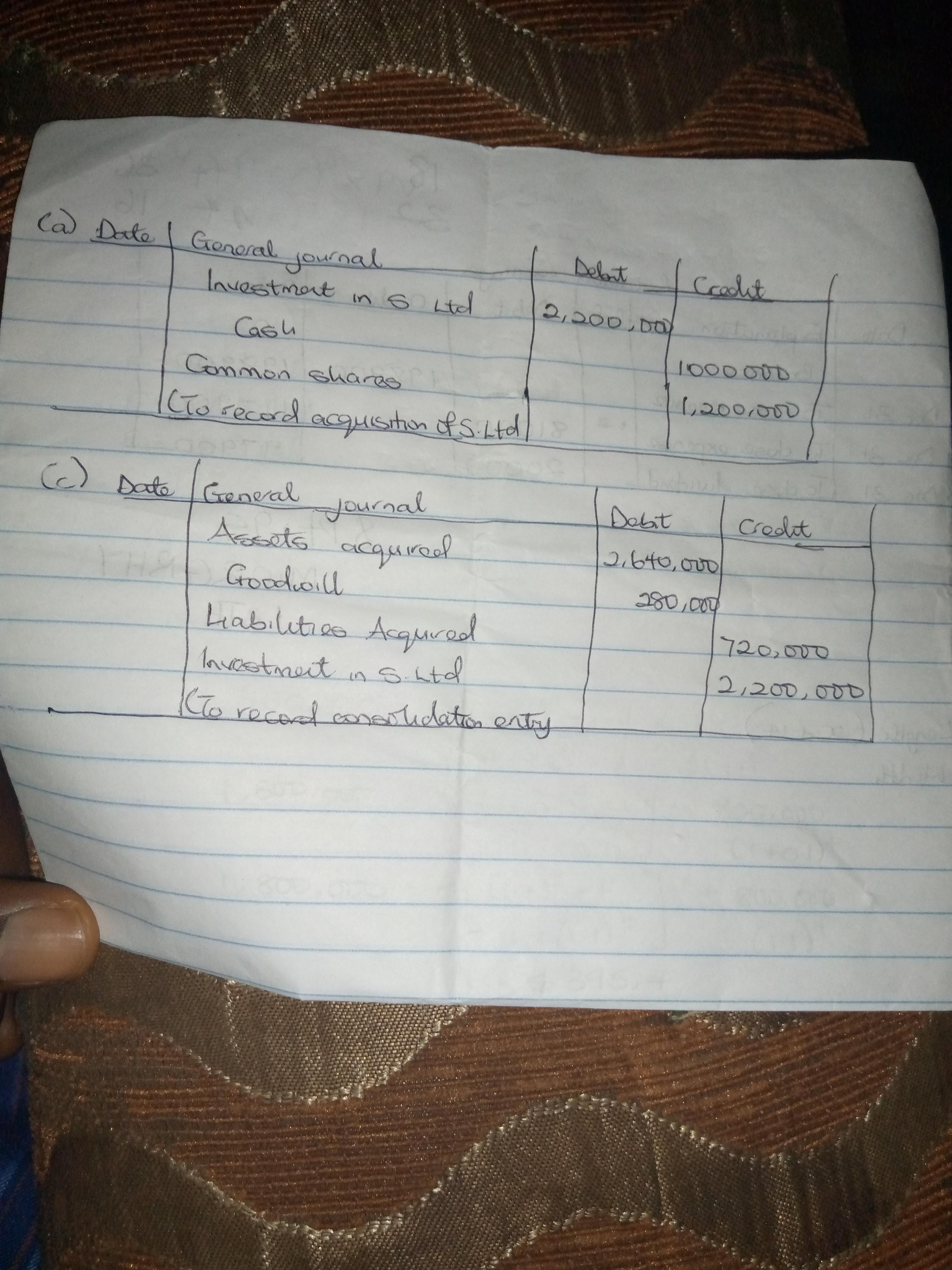

Answer: See attachment

Explanation:

Check the attachment

For (a),

Common shares = $800,000 × 1.5

= $1,200,000

b. Fair value of assets = $2640000

Less: Fair value of liabilities = ($720000)

Net value of S. Ltd = $1920000

Purchase consideration = $220000

Goodwill on acquisition = $2,200,000 - $1,920,000 = $280,000

d. Fair value of assets acquired = $2,640,000

Less: fair value of liabilities acquired = ($720,000)

Net value of S. Ltd = $1,920,000

Purchase consideration = 1,000,000 + (400,000 × 1.5) = 1,000,000 + 600,000 = 1,600,000

Bargain purchase = $1,920,000 - $1,600,000 = $320,000

See attachment for further explanation