Money clothes business and shoes hope this helps

Answer:

Consider the following explanation

Explanation:

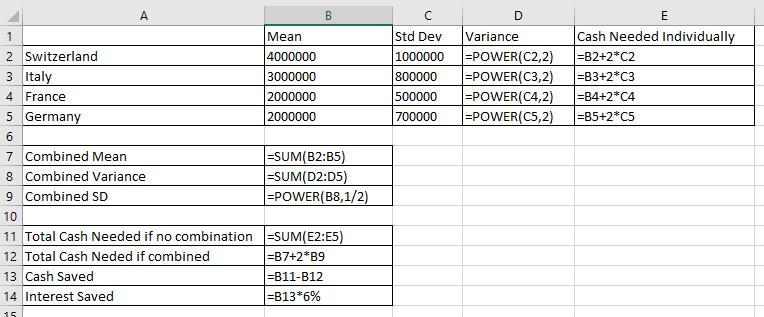

Please note that if cash requirements are combined, mean requirement of combined entity can be simply summed up, but same is not true for standard deviation as it is not additive.

So first we need to calculate the variance by taking square of SD, then we sum it for all the location to get variance of combined entity and then we take square root again to get the SD of combined entity.

Keep in mind that we can take a simple summation of variance due to the fact that requirement in different locations are independent of each other and their correlation coefficient is = 0.

Solution is given through following image sheet -

Answer:

para po, pag gipit Tayo meron tayong makukuha na saving

Explanation:

sana po makatulong po Ito at pa ki brain less din po

Answer:

The break even level of units per month fall by 16 units.

Explanation:

The current breakeven units per month are,

Break even in units = 5600 / (20 - 6)

Break even in units-March = 400 Units

The fixed costs remain constant in the short run to a certain activity level so assuming that the fixed costs will remain $5600.

The new variable costs will be 6 * 0.9 = $5.4

Assuming everything else remains constant,

The new break even in units per month = 5600 / (20 - 5.4)

New break even in units = 383.56 rounded off to 384 units

As a result of decrease in the variable cost per units, the new break even point becomes 16 units less than the previous one.

The condition of uninsured people in the United States is very well written in the paragraph where it highlights the fact that uninsured people are less likely to receive care and more likely to have poor health status.

<h3>

What do you mean by medically uninsured?</h3>

In the US, more or less than 50 million do not have health insurance, and an additional 10-20% of people do not have insurance.

Uninsured are not eligible for Medicaid, which is the safety net for most Americans, because they do not qualify for country-based benefits, dependent assistance families, or do not meet other financial or class conditions.

The financial burden of medical care is high on uninsured individuals. It is told that most of them disappear as they do not have enough money to cover the high medical expenses.

Thus, we can say that uninsured people are less likely to receive care and more likely to have poor health status due to lack of finance.

To learn more about medically uninsured, refer to the link:

brainly.com/question/25793763