A shift to the right (or outward) in a ppc/ppf represents expansion, which may be brought about by better utilizing current resources (improved technology) or by gradually acquiring more resources.

The Production Possibility Frontier (PPF): What Is It?

The production possibility frontier (PPF) is a graphed curve that shows the possible output of two items whose production is reliant on a single finite resource. The PPF is often referred to as the production possibility curve.

PPF is important in economics as well. For instance, it can show that a country's economy has achieved the maximum level of effectiveness.

to know more about Production Possibility Frontier (PPF)

brainly.com/question/26754295

#SPJ4

Car salespersons are notorious for using the lowball technique, which involves changing terms after an agreement has been made.

Answer:

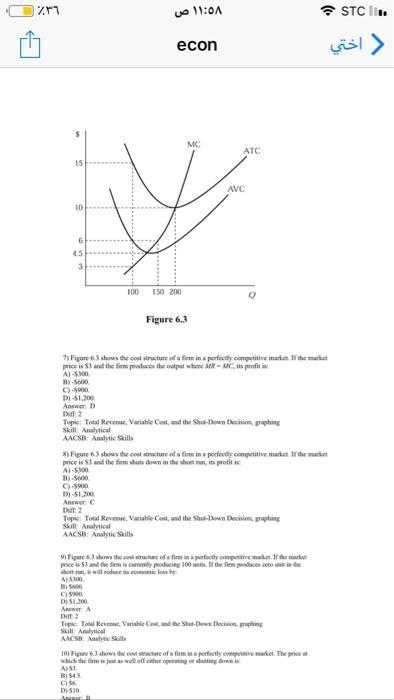

$10 for 200 units which means $0.05 per unit.

Explanation:

The firm will only survive in a perfectly competitive market if its average cost is at minimum level which we can see in the figure. The lowest average cost is $10 for 200 units which means average cost per unit is $0.05 per unit. At this stage the company will be able to produce higher profits because its average cost per unit is at minimum level.

Answer:

The amount allocated to ending inventory is $ 11,520

Explanation:

Using LIFO basis of inventory valuation implies that the items received last are sold first,in other words, sales of 160 units comes from the purchases of 240 units made on July 5,that leaves 80 units of the purchase in closing inventory.

However,the sale of 140 units on 30 July is taken from purchases of 120 units on July 21 as well as purchases of July 5.

The amount allocated to ending inventory is computed below:

July 5 60 units at $112 $6,720

opening inventory 40 units at $120 $4,800

Value of closing inventory $11,520