Answer:

$0

Explanation:

Given that,

Total revenues = $4,000,000

Cost of goods sold = $3,500,000

Depreciation expense = $500,000

Interest expense = $120,000

Earnings before interest and taxes (EBIT):

= Total revenues - Cost of goods sold - Depreciation expense

= $4,000,000 - $3,500,000 - $500,000

= $0

Therefore, the EBIT for a firm is $0.

The major financial change between post ww2 borrowers and borrowers after 1970 was that there were plenty of jobs after World War 2 and the economy was growing at a large extent.

Most of the people believed that their income would not change even though there were plenty of jobs in the economy.

However they all have a constant income from the year 1945 to 1970.

So all the people continued to borrow more and more money by not attending or joining any post war job in the economy.

Banks were also willing to lend more and more money as they were on the way of high earning through more lending but they get closed.

So after the war people continued to increase their loans and debt ratio in the economy of lending due to which it became the period of great depression.

To know more about post war borrowing here:

brainly.com/question/2675965

#SPJ4

None of the above

Explanation: The network structure is a newer type of organizational structure viewed as less hierarchical (i.e., more "flat"), more decentralized, and more flexible than other structures. In a network structure, managers coordinate and control relationships that are both internal and external to the firm.

Answer:

The correct answer is letter "C": informal leader.

Explanation:

Informal leaders are individuals to whom people put their trust on because they provoke a strong influence within a group or because others see that individuals as examples to follow. However, informal leaders are not officially recognized. Most formalized leaders begin naturally being informal leaders until the collective will of subordinates place them in the position of power.

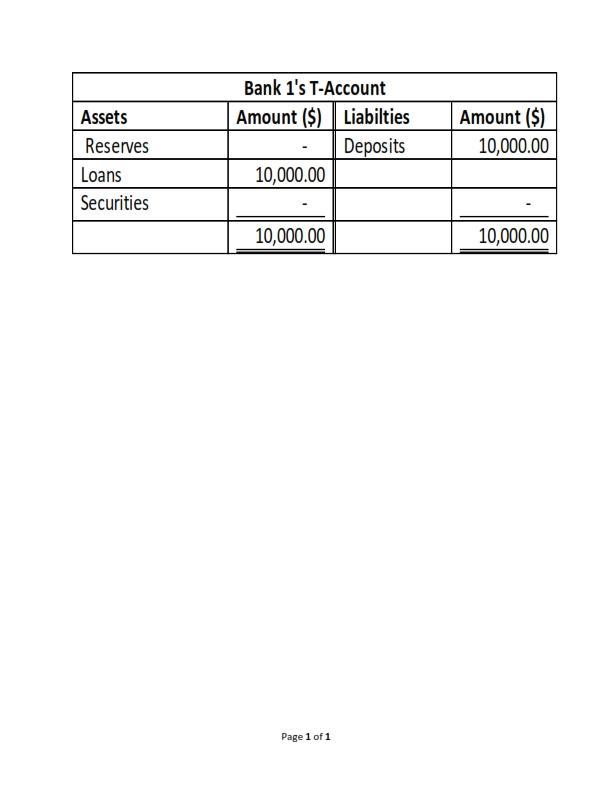

Answer:

1. Assets is debited for $10,000 as loans.

2. Liabilities is credited for $10,000 as deposits.

Explanation:

Note: This question is not complete as the amount is omitted. The complete question is therefore presented before answering the question as follows:

Suppose banks keep no excess reserves and that all banks are currently meeting the reserve requirement. The Federal Reserve then makes an open market purchase of $10000 from Bank 1.

Use the T-account below to show the result of this transaction for Bank 1, assuming Bank 1 keeps no excess reserves after the transaction.

The explanation of the answer is now given as follows:

Note: See the attached photo for Bank 1's T-Account.

In the attached photo, we can see that:

1. Assets is debited for $10,000 as loans.

2. Liabilities is credited for $10,000 as deposits.