Please state these fees please?

Answer:

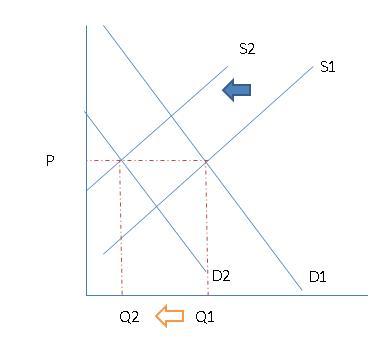

The equilibrium quantities of lettuce reduces and price remains the same.

Explanation:

In the attached image is the grapichal analysis of the reduction of demand and supply in the same proportion.

Answer: a. an e-brand brand

Explanation:

An e-brand is one that provides just an online service for merchandise sales. These companies do not have physical locations but rather show you all that they sell on their websites and then when you purchase something, they deliver it as a physical good. The most popular example of such is Amazon.

The advantage of such brands is that they get to save on the rental and other property costs related to establishing brick-and-mortar stores because they are online.

Answer:

Explanation:

Direct Material $165,000 (195,000 - 30,000)

Direct labor $110,000 (150,000 - 40,000)

Overhead $165,000 ( 110,000 * 150%)

Total cost $440,000

Work in progress transfer = $15,500 + $440,000 - $27,000 = $428,500

Answer: Company’s break-even point in unit sales is <em><u>3900 units</u></em>

Explanation:

Given :

Selling Price (SP) = $ 15.70

Variable expense per unit (VC) = $10.30

Fixed expense = $21,060

Now,

Contribution per unit = SP - VC = $15.70 - $10.30 = $5.40

Break-even point in unit sales is given as :

=

= 21060/5.40

=3900 units