The risk a company takes every time a company hires a new employee and trains them to take on the new role is known as financial risk.

<h3>What is a risk?</h3>

Risk can be defined as a possibility or a situation which is uncertain and involves exposure to danger. A risk from an investment perspective is the possibility of incurring losses due to market uncertainties.

When a company hire new employee, the company would expend some cost towards training of the newly recruited employee; which is termed financial risk.

Hence, the risk a company takes every time a company hires a new employee and trains them to take on the new role is known as financial risk.

Learn more about risk here : brainly.com/question/1224221

Answer:

The correct answer is defined contribution plan.

Explanation:

The defined contribution plan is a pension plan in which the company agrees to make monetary contributions each year for the benefit of the employee.

Generally, in a defined contribution plan the employee has the right over the invested assets and is free to withdraw the accumulated funds if his retirement occurs prematurely. For this reason, the defined contribution plans are said to have portability, that is, if the employee ends his employment relationship with the company, he can transfer his funds to his new company's pension plan or to a private pension plan.

Upon retirement, the employee can access the accumulated funds, but unlike in the defined benefit plans, no amount is guaranteed. The investment risk is assumed entirely by the employee.

For example, the company can contribute 1% of salary to a pension fund every month. The employee can also contribute part of his salary to this plan.

Answer: Please refer to Explanation

Explanation:

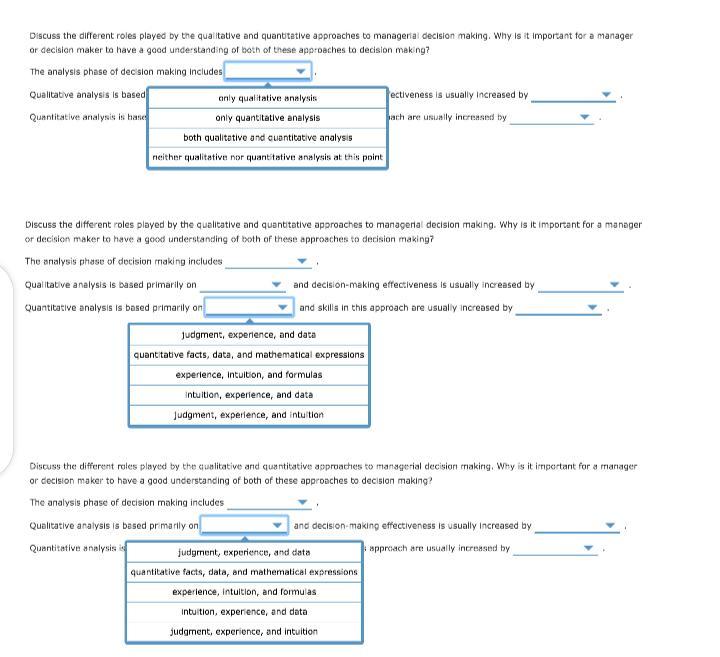

The attached photo contains the complete question as well as some options.

1. Both qualitative and quantitative analysis.

The analysis phase includes both of these types of analysis to provide a complete view of a variable from both a numbers and an experience perspective.

2. Judgement, experience, and intuition.

Qualitative Analysis is usually based on these 3 as numbers are not necessarily used.

3. Experience.

The more you are faced with analysing Qualitative data, the more the get used to it and better at it.

4. quantitative facts, data, and mathematical expressions.

Quantitative Analysis is done on mathematical instruments such as facts,data and expressions to provide a more mathematical driven approach to analysis.

5. Studying.

The more you study Quantitative Data and it's methods of analysis, the better you get at it because you begin to see patterns as well as use better analytic tools.

Business services are expense items that do not become part of a final product.

Business services are intangible items such as IT, finance, management, shipping and more. These services support each other but do not become part of the final product. Installations and supplies are both part of the final product. Supplies to build and installations to put together.

Answer:

B) produce more output with the same inputs.

Explanation:

Hicks-neutral technical is a theory by

John Hicks and can be explained as a change in the function of the production of a particular business with respect to the neatral condition of economic system at that period. It should be noted that Neutral technical progress allows a firm to produce more output with the same inputs.