Answer:

Please find the complete question in the attachment.

Explanation:

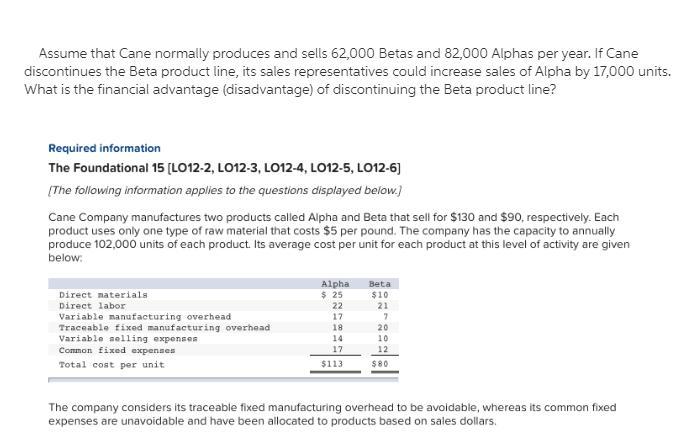

the margin of contribution unit

the margin of contribution unit

Margin Contribution Unit

Margin Contribution Unit

8

Contribution losses

Fixed cost avoidable

The margin of Alpha contributions

Fiscal benefits (disadvantage)

Answer:

-UNICEF Việt Nam – Quỹ Nhi đồng Liên Hiệp Quốc

– UNFPA – Quỹ Dân số Liên Hợp Quốc

– UNIDO – Tổ chức Phát triển Công nghiệp Liên Hiệp Quốc

– Aide et Action International

– IntraHealth International

– The Asia Foundation

Explanation:

Tổ chức phi chính phủ phủ là tổ chức quốc tế trong đó các thành viên tham gia không phải là chính phủ, tổ chức phi chính phủ được thành lập một cách tự nguyện, hợp pháp không vì lợi nhuận, thúc đẩy sự phát triển trong công nghệ, khoa học kỹ thuật…

Answer:

Thomas Edison

Explanation:

Thomas Edison early life was very normal. He was born in a poor family. His mother was a school teacher. Thomas Edison did not get recognition until he was successful in inventing the bulb. He did many experiment which failed and no one supported him during this era. He continued his hard work and finally his one of experiment became successful and he invented a bulb. The world then recognized his efforts and made him a hero. His recognition was only based on the success of his experiment and the marketplace.

Answer: $369,500

Explanation:

The Cost concept of accounting calls for the recording of Assets at their cost.

Clementine Repair services offered to buy the land at $350,500 when it was priced at $388,500.

The seller countered with $369,500 and Clementine accepted this.

This means that Clementine bought the land for $369,500 which makes it the cost price.

They should therefore record it at $369,500.