Answer:

Bond Price = $5,300,862.264 rounded off to $5,300,862.26

Explanation:

To calculate the price of the bond today, we will use the formula for the price of the bond. Assuming the bond is an annual bond, the semi coupon payment, number of periods and semi annual YTM will be,

Coupon Payment (C) = 6,000,000 * 0.06 * 6/12 = 180

,000

Total periods (n) = 8 * 2 = 16

r or YTM = 0.08 * 6/12 = 0.04 or 4%

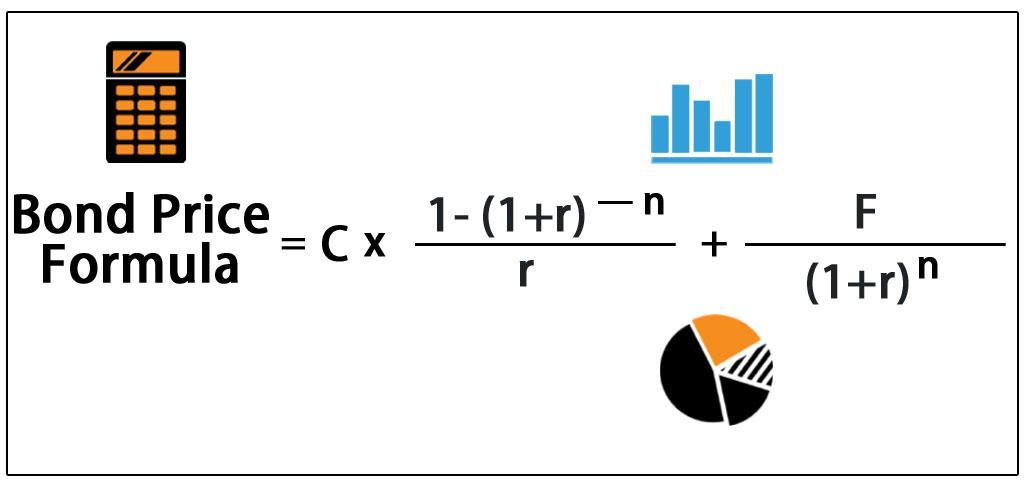

The formula to calculate the price of the bonds today is attached.

Bond Price = 180000 * [( 1 - (1+0.04)^-16) / 0.04] + 6000000 / (1+0.04)^16

Bond Price = $5,300,862.264 rounded off to $5,300,862.26