Answer:

terrible and no i am not failing

Explanation:

someone go check out my recent question i need help asap

Answer:

<u><em>Radical change</em></u>

Explanation:

A distinguishing feature of radical change is that it is rapid in terms of ground breaking breakthrough innovations.

Thus, In 1993 the film industry was experiencing breakthrough innovations such as the release of the blockbuster movie "Jurassic park" which introduced high-tech special effects in the film industry.

Interest on purchase consideration, the salary of partners, and interest on vendor capital are to be charged during the pre-incorporation period.

Answer:

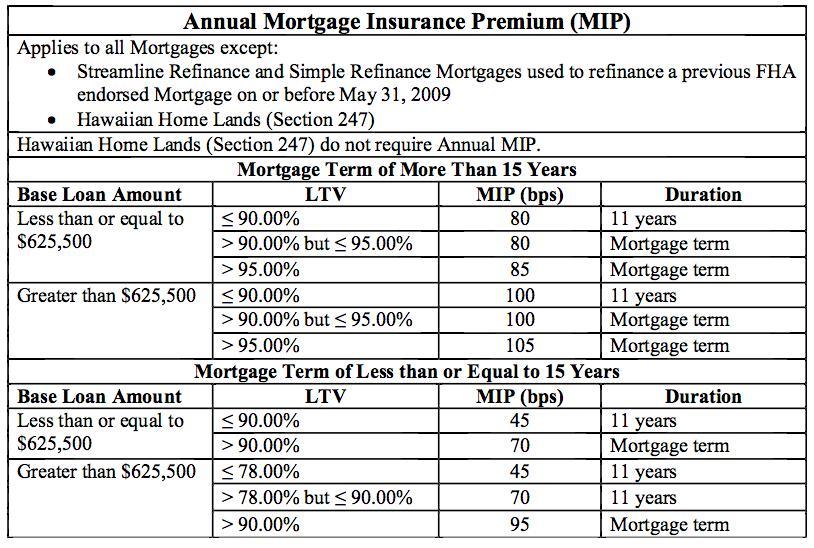

prime mortgage insurance (PMI) is an insurance that mortgage lenders require when borrowers make a down payment of less than 20% of the purchase price of the house.

We are not given any table, so I looked in the internet to find one that can be used as an example:

outstanding principal = $142,000 - 17% = $117,860

- mortgage term equal or less than 15 years

- base loan amount is less than $625,000

- loan to value ratio = 1 - down payment = 83%, which means it is ≤ 90%

- bps = 45

total yearly premium = principal x bps = $117,860 x 0.0045 = $530.47

monthly PMI payment = $530.47 / 12 months = $44.20