Answer:

Monthly deposit= $810.20

Explanation:

Giving the following information:

Number of periods (n)= 18 months

Interest rate (i)= 0.04/12= 0.0033

Future value (FV)= $15,000

<u>To calculate the monthly deposit, we need to use the following formula:</u>

FV= {A*[(1+i)^n-1]}/i

A= monthly deposit

Isolating A:

A= (FV*i)/{[(1+i)^n]-1}

A= (15,000*0.0033) / [(1.0033^18) - 1]

A= $810.20

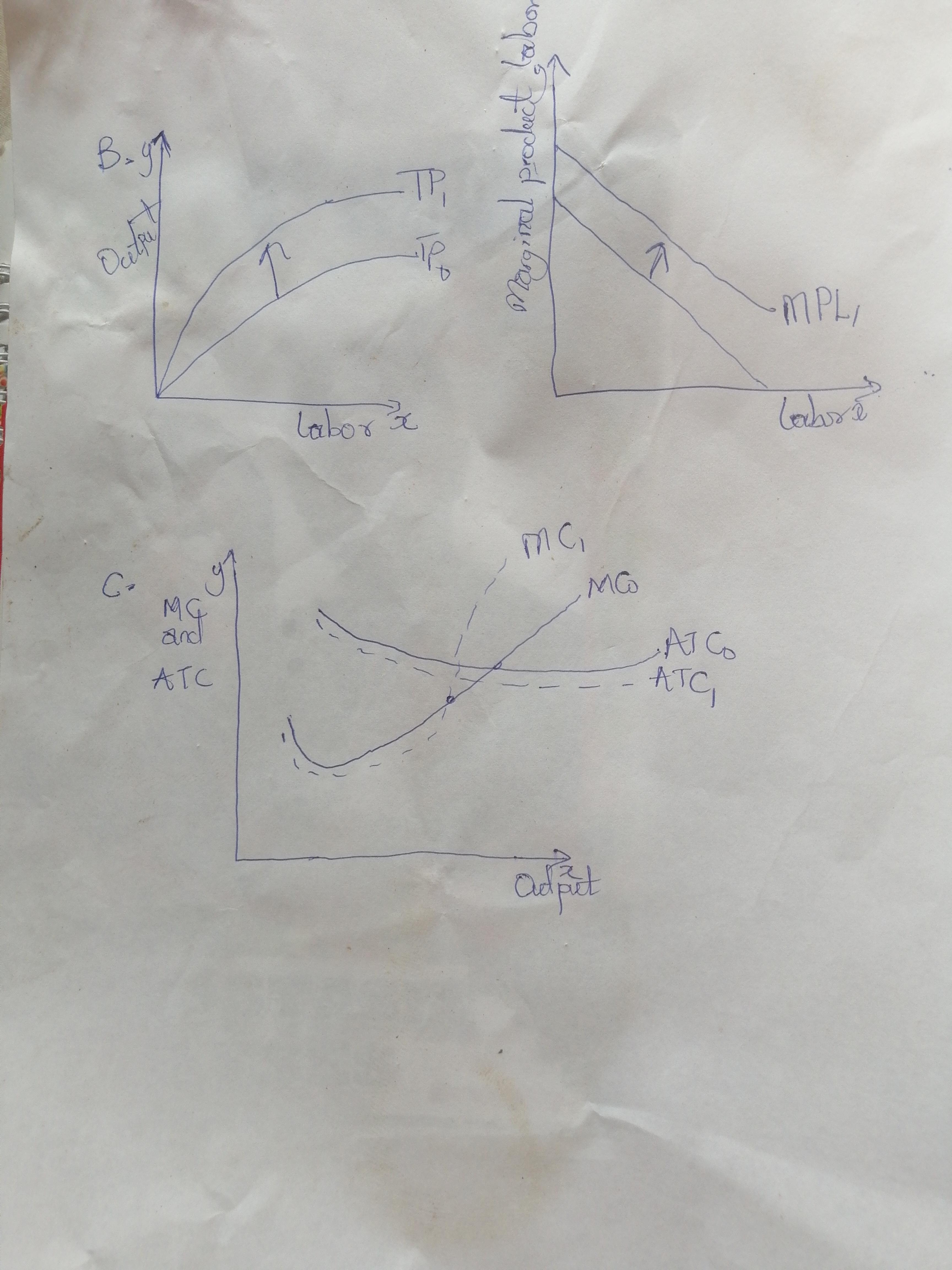

Answer: Labor cost is a representative of greater percentage of total cost for many firms. From the data of Bureau of Labor statistics, the U.S labour cost up to 2% in 2015 in comparison to 2014.

Explanation:

A. As labor increases, average total cost and marginal cost increases as well due to the fact that labor is part of total cost of production. If labor cost represents only variable cost when firms shut down, labor cost will be save but if it represents but variable and fixed cost, labor cost can't be avoided.

B. A positive productivity growth lead to a total product curve and marginal labor curve shift upward because total output and marginal product of labor curve increases.

C. A positive productivity curve will result in an downward shift of marginal cost curve and average total cost curve because average total cost and marginal cost decreases per output.

D. If labor cost are rising overtime on average. equipments, technologies and methods that increases labor productivity will be adopted in order for total output and marginal product of labour to increase.

False, any leader should have good listening skills regardless of their political party

Odd consecutive integers are odd integers that follow each other. They have a difference of 2 between every two numbers. If n is an odd integer, then n, n+2, n+4 and n+6 will be odd consecutive integers. the first number in the pattern is always the variable on its own or in this case, "n". Examples.