Answer:

The market price of an unrestricted share of the same stock.

Explanation:

Restricted stock units (RSU) are defined as a type of compensation in shares that an employer will give to an employee.

Usually certain conditions or performance should be met before the employee gets this benefit. For example staying with the company for a number of years.

A vesting plan of distribution schedule is used to allocate the shares.

The value of the compensation will be the number of shares given by the RSU multiplied by the market value of unrestricted share of the same stock.

For example if an employee has RSU of 1,000 shares, and share value is $10

Value of RSU compensation = 1,000 * 10 = $10,000

Answer:

Depreciation expense $12,910

Book value $46,680

Explanation:

Kansas Enterprises

Formula for Depreciation expenses

Annual depreciation expense=(Cost-Residual value)/Useful Life

Where,

Cost = 72,500

Residual value =7,950

Useful life = 5 years

Let plug in the formula

=(72,500-7950)/5

=64,550/5

=$12,910/year

Therefore depreciation expense for 2021

=$12,910

Calulation for Book value

Book value = $72,500 – ($12,910× 2)

$72,500 -$25,820

=$46,680

Therefore the book value would be $46,680

C. The tools and processes that surround us to gather and interpret data can be defined as an information technology environment.

Our environment is what surrounds us - so if the environment is technological, then different types of technologies and tools are what fall under that category.

Answer and Explanation:

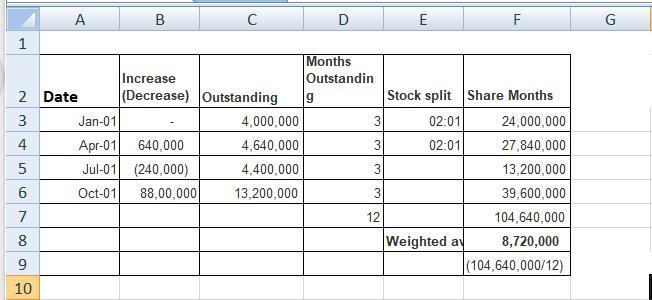

a. The computation of the weighted average number of shares is shown in the attachment below:

b. Now the earning per share i.e EPS

= (Net Income - Preferred Dividend) ÷ (Weighted average number of shares

)

= ($9,850,000 - $10,000) ÷ (8,720,000 shares)

= $1.13

The preference dividend is

= (2,000 × $100 × 5%)

= $10,000

Answer: I hate Trump and would make him eat tortilla chip vertically :/

Explanation: