I would say false, the sheet that reports the revenues and the costs is known as the income statement. the balance sheet is the sheet that would report all of the assets (such as the cash, accounts receivable, or others). The balance sheet will also report all the liabilities (including the accounts payable, notes payable and others). Lastly, the balance sheet will also report the equity or the capital account of the business. So in a nutshell, the balance sheet reports the assets, liabilities, and owner's equity.

Answer:

The answer is "21,622.98".

Explanation:

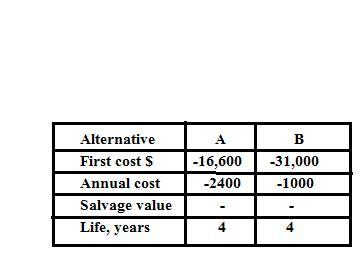

In the given question some information is missing, which can be defined in the given attachment.

To calculate the first cost we first subtract B cost is to X.

NPV = Cash Flow of the sum of PV amount

The value of Option A or NPV = -24,575.88

The value of Option B or NPV:

The value of Option B or NPV = -X -2952.9

As demanded

In Option B the value of NPV = In Option A the value of NPV

Personal finance is a term that covers your money management as well as saving and investing. These contain the budget, banking, insurance, mortgage, investments and retirement, tax, and estate planning. The term often directs to the entire industry that delivers financial services to people and homes and recommends financial and investment options.

Personal dreams and wishes - and plan to fulfill those essentials in your financial obstacle - also influence how you get the above. In order to use your earnings and savings most, it is necessary to be economical. Personal finance helps you learn the difference between good and bad suggestions and make intelligent financial conclusions.

Learn more about Personal finance:

brainly.com/question/28066148

#SPJ4

Answer:

The first method would use prefabricated building segments, would have an initial cost of $6.5 million.