Answer:

240,000,000

Explanation:

Each year you would need to invest 240,000,000 into the saving account over a period of five years to get to the desired amount. If they are only putting in 12%of the retirement funds that would 14,400,000 and that would take about 8 years.

Answer:

a and b

Explanation:

Religious orientation has nothing to do with how much money to spend or what machine to use

Answer:

conduits

Explanation:

A mortgage-backed security is one in which is similar to bonds but that usually consists of home loans ought from banks that issued them. It is a type asset-backed security which can be sold through brokers.

investment in mortgage-backed assets means the investor is lending out his money to people that intend to get a home.

A mortgage-backed security can be bought directly from banks or through brokers. These brokers are also called conduits.

Cheers

A certificate of deposit (CD) would be the best banking

choice when the interest rate is determined ahead of time and there is an

assurance to get back what you put in plus interest once the CD matures. If you leave the money alone during the

investment period then the bank will pay you an interest rate slightly higher

than what you would have earned in a money market or checking account. Thus,

all gains from certificate of deposits are taxable as income unless they are in

a tax-deferred (IRA) r tax-free (Roth IRA) account.

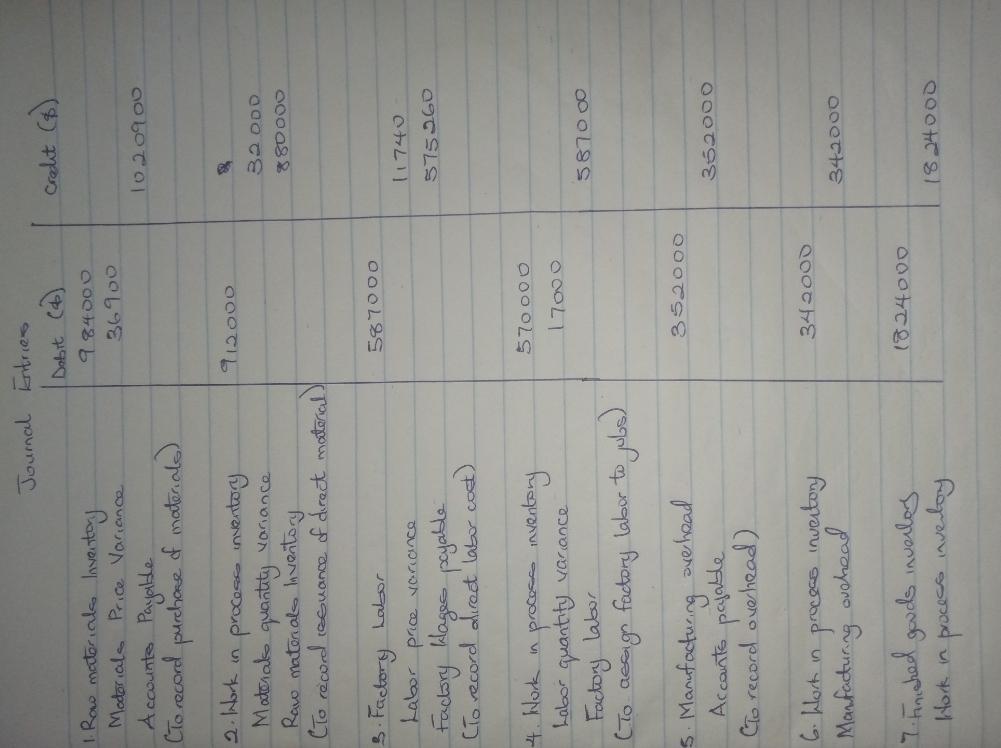

Answer: See explanation

Explanation:

AP = 4.15

SP = 4.0

SQ = 114000 × 2 = 228000

1. Direct Materials Price

= (AQ × AP) - (AQ × SP)

= (246000 × 4.15) - (246000 × 4.0)

= 1020900 - 984000

= 369000 U

2. Direct Materials Quantity

= (AQ × SP) - (SQ × SP)

where SQ = 114000 × 2 = 228000

= (220000 × 4.0) - (228000 × 4.0)

= 880000 - 912000

= 32000 F

3. Direct Labor Price

= (AH × AR) - (AH × SR)

= (58700 × 9.8) - (58700 × 10)

= 575260 - 587000

= 11740

4. Direct Labor Quantity

= (AH × SR) - (SH × SR)

where, SH = 114000 × ½ = 57000

= (58700 × 10) - (57000 × 10)

= 587000 - 570000

= 17000 U

5. Total Overhead Variances

= 352000 - (57000 × 6)

= 352000 - 342000

= 10000 Unfavorable

Check attachment for further details