Answer: Check attachment and explanation.

Explanation:

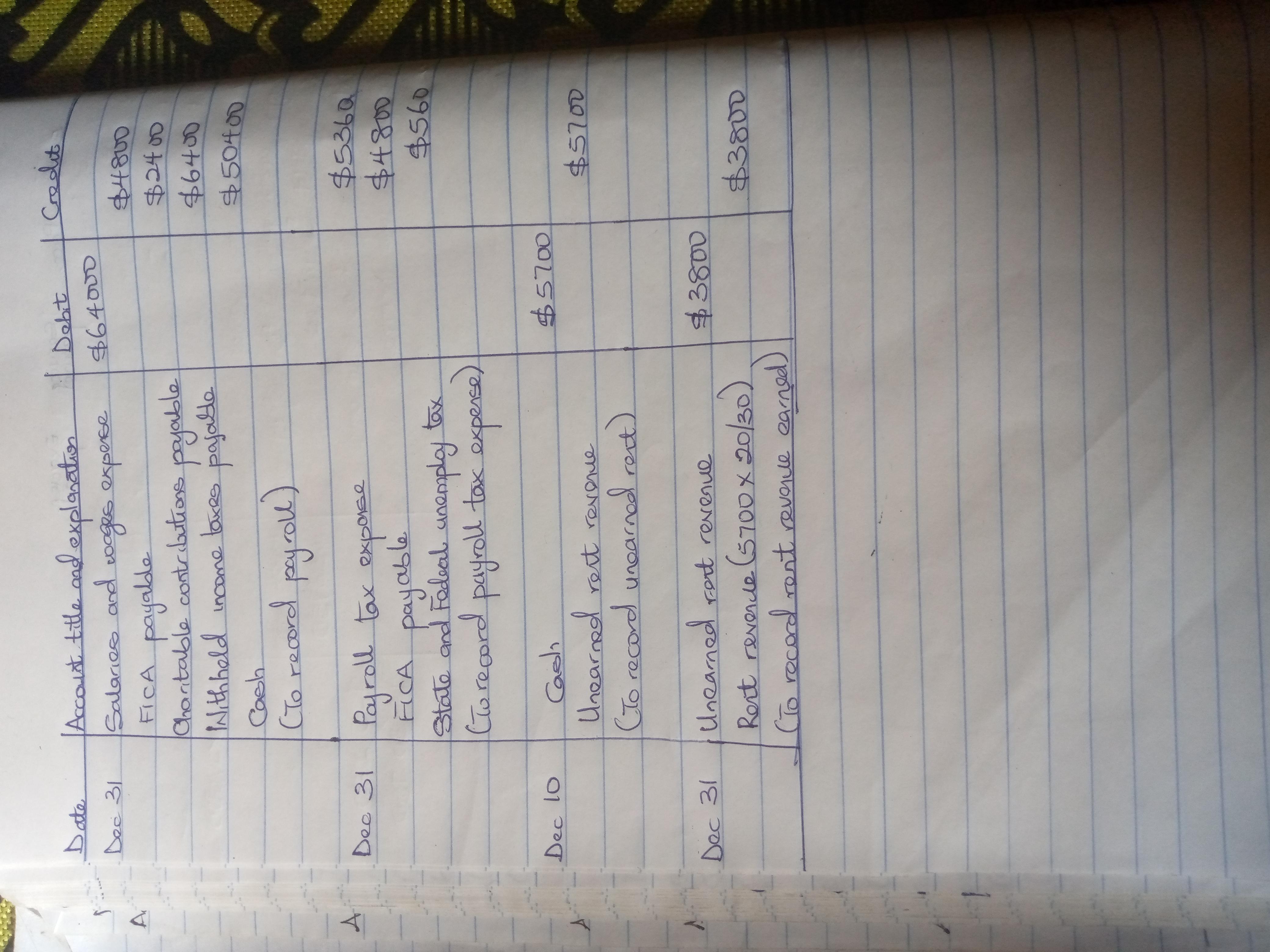

a. The question has been solved. Check the attachment.

b. LAKEVIEW COMPANY

Balance sheet (Partial)

December 31

Current liabilities

FICA Payable=$4800 + $4800= $9600

Charitable contribution payable = $2400

Withheld income tax payable = $6400

State and Federal unemployment tax payable = $560

Unearned rent revenue = $5700 - $3800 = $1900

Total current liabilities = $20860

The change in consumption resulting from a change in real income !

Give thanks if correct!

Answer:

The answer is B.Effectiveness.

Explanation:

Effectiveness is accomplishing tasks that help fulfill organizational objectives.

Answer:

Yes, Sarah can revoke the gift to her friend.

Explanation:

Gift is the transfer of property from one person, usually the donor(giver) to another person, donee(receiver) without expecting any thing like compensation in return. Gift can be given or transfered to either an individual or organization.

A gift can be revoked by the donor in law. Such gift is called Causa Mortis Gift.

Causa Mortis Gift is a gift given or transfered in expectation of death of the donor. Where a donor gives out his/her gift during the course of undergoing major surgery, such could also be called Causa Mortis Gift. This type of gift can be revoked anytime before the donor's death or recovery from surgery or illness and cannot be revoked after his/her death.

The acquisition of caremark rx, inc. , (a pharmacy benefits manager) by cvs corporation (a retail pharmacy) is an example of a <u>backwards vertical acquisition </u>and allows cvs to gain<u> increase market power</u>.

The American healthcare firm CVS Health Corporation (formerly CVS Corporation and CVS Caremark Corporation) is the owner of numerous brands, including Aetna, a health insurance provider, CVS Caremark, a chain of retail pharmacies, and CVS Pharmacy.

The specialized pharmacy section known as CVS Specialty offers specialty pharmacy services to people with hereditary or chronic disorders who need sophisticated and expensive pharmacological treatments.

The largest specialty pharmacy in the United States is CVS Health, which runs 24 retail specialty pharmacy shops and 11 specialized mail order pharmacies.

To learn more about CVS here

brainly.com/question/27929890

#SPJ4