Answer:

Refer explanation and diagrams

Explanation:

A. Two functions of price:

a. Signalling function: Changes in price helps producers and consumers understand changes in market conditions. For example, when there is high demand for a product, the price will increase, signalling suppliers to produce more. On the other hand, when there is excess supply, this would be eliminated by causing the market price to fall, Prices are adjusted to help determine where resources are required and where they are not.

b. Rationing function: Resources in the economy are limited and shortages are bound to occur. Prices help ration these scare resources when demand exceeds supply. When there is a shortage, prices will rise and only those who are wiling and able to purchase at the new price will consume the product, others will deter and fall back being unable or unwilling to afford. One example are auctions, where prices are bid up until demand falls enough to level the availability of a product and it is sold to the highest bidder/bidders.

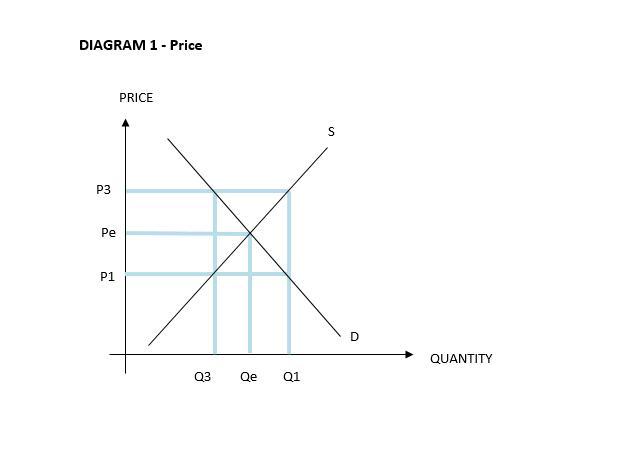

B. Price in an economy is determined by: the interaction of quantity demanded and quantity supplied, creating the equilibrium price (refer Diagram 1). At price P1, quantity demanded exceeds quantity supplied which would create a shortage of Q3 to Q1. At price P3, quantity supplied exceeds quantity demanded, causing a surplus of Q3 to Q1. However, at price Pe, quantity supplied is equal to quantity demanded (Qe), creating neither a surplus nor shortage and this price is determined in the market economy.

C. When the government interferes in a market, the following can happen:

a. Surpluses or shortages

b. Consumer and producer surplus would not be maximized

c. Deadweight loss is created

d. National welfare compromised

Two common ways of government intervention are through price floors and price ceilings. In the example provided in the Diagram 2, a price floor is imposed in the form of a minimum price on wheat to protect wheat farmers from low prices.

a. Surplus created: At the free market equilibrium, price is Pe and quantity supplied equals quantity demanded of Qe. However, when the government sets the price at P3, quantity supplied rises to Q3 and quantity demanded falls to Q1 which creates a surplus of wheat from Q1 to Q3, a waste of valuable resources.

b. Consumer and producer surplus not maximized: At the free market price of Pe, consumer surplus is the triangular area of A-Pe-X and producer surplus of the triangular area B-Pe-X. When the price is raised, consumer surplus falls to area A-Y-P3 and producer surplus falls to area Y-Z-B-P3.

c. Deadweight loss: This change in producer and consumer surplus creates a deadweight loss of the triangular area X-Y-Z.

d. National welfare is also compromised as the producer and consumer surplus are reduced and a deadweight loss is created.