Barry Goldwater is willing to get the U.S. involved with the

nuclear warfare. Barry Goldwater is known to be an American politician and a businessman

of which he had a five term of being a senator in the united states from Arizona.

<span>Because the statute penalizes the person committing the crime as well as the employer whose employee committed the crime, Chris can be held liable, and the company that we works for (Watkins) can be held vicariously liable under the statute.</span>

Answer

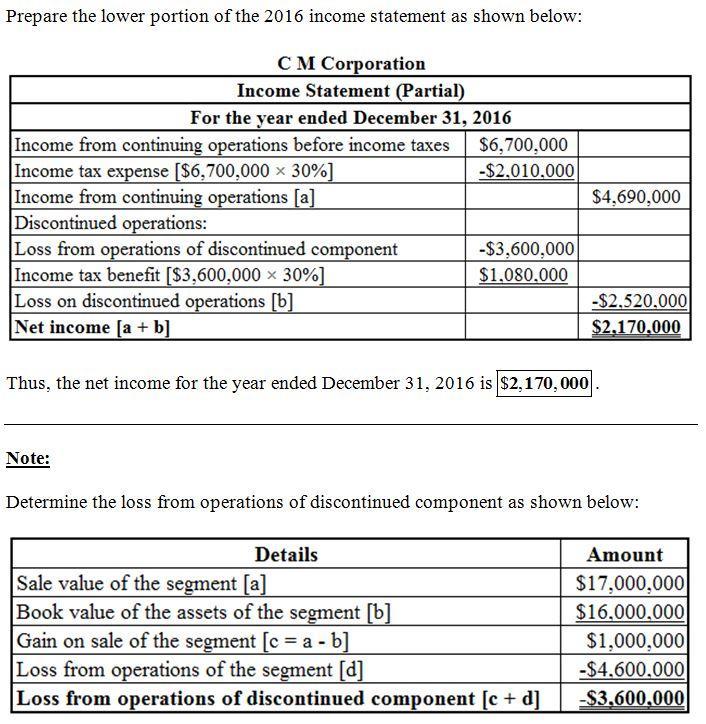

Net income = 2.170.000

Loss from operations of discountinued component = -3.600.000

The answer and procedures of the exercise are attached in a microsoft excel document.

Explanation

Please consider the data provided by the exercise. If you have any question please write me back. All the exercises are solved in a single sheet with the formulas indications.

Answer:

Date Account Titles Debit Credit

Oct 1 Cash $16,800

Common Stock $16,800

Oct 2 No journal entry - -

Oct 3 Office Furniture $2,500

Accounts Payable $2,500

Oct 6. Accounts Receivable $3,

400

Service Revenue $3,400

Oct 27 Accounts Payable $1,100

Cash $1,100

Oct 30 Salaries Expense $2,650

Cash $2,650