Answer:

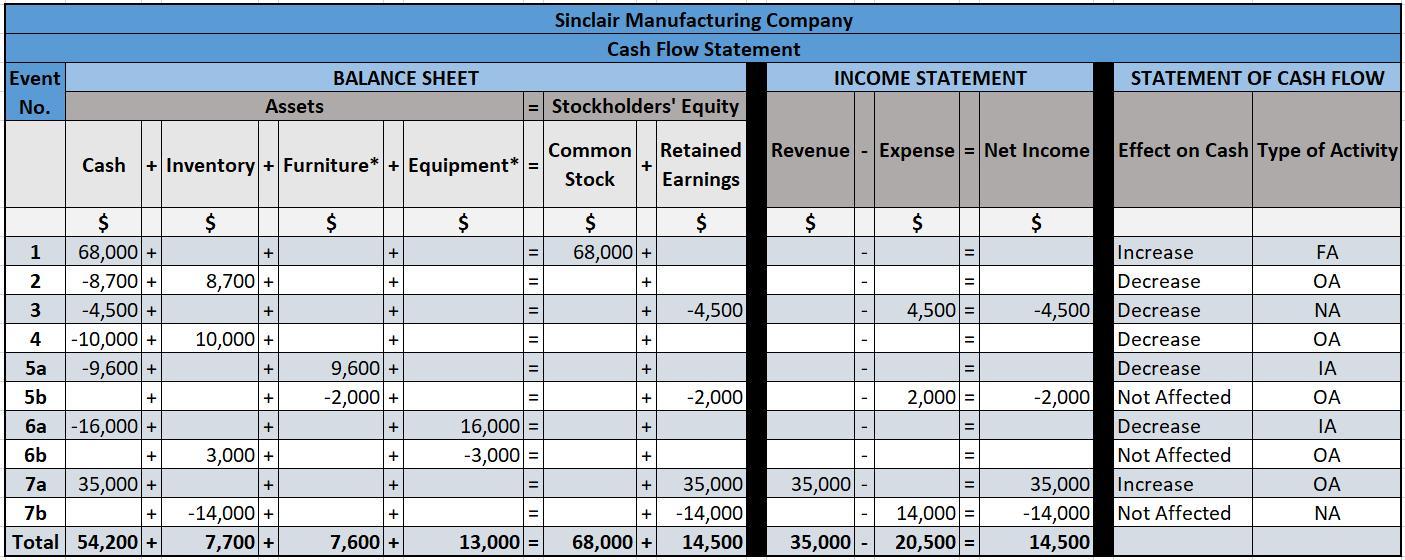

Please see the attached image for the Horizontal Financial Statements of Sinclair Manufacturing Company.

Explanation:

5. FURNITURE - Straight Line Method

Book Value of Furniture = Cost of Acquisition - Residual Value

Cost of Acquisition = $9,600

Residual Value = $1,600

Book Value of Furniture = $9,600 - $1,600

Book Value of Furniture = $8,000

Useful Life = 4 years

Depreciation Expense = $8,000 / 4 years

Depreciation Expense = $2,000 per year

6. EQUIPMENT - Straight Line Method

Book Value of Equipment = Cost of Acquisition - Residual Value

Cost of Acquisition = $16,000

Residual Value = $1,000

Book Value of Furniture = $16,000 - $1,000

Book Value of Furniture = $15,000

Useful Life = 5 years

Depreciation Expense = $15,000 / 5 years

Depreciation Expense = $3,000 per year