Answer:

Denominator

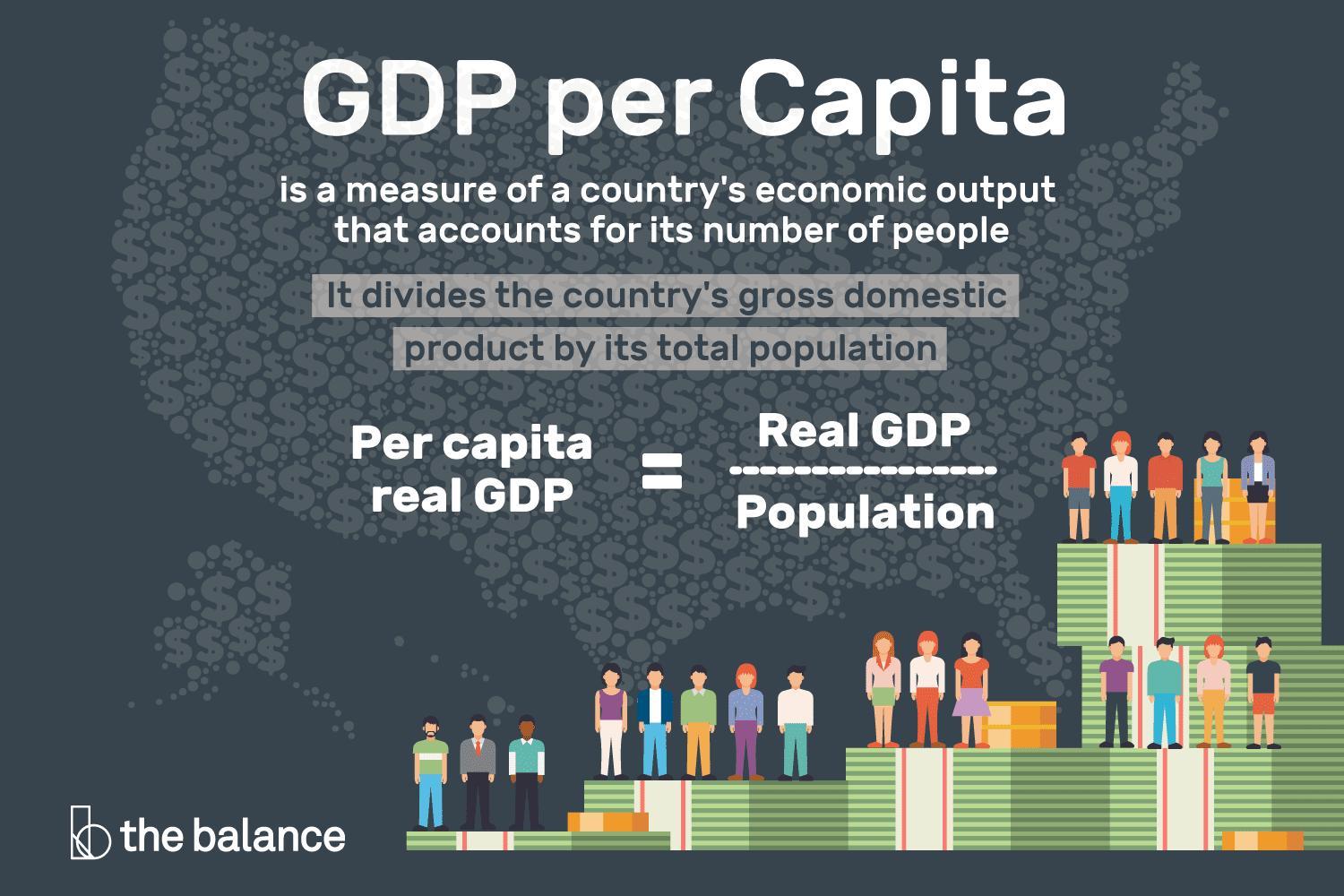

Lower

Numerator

Explanation:

The reason is that the statement is talking about the low per capita GDP which we can see in the picture attached with this answer.

We can see that if the denominator is lower which means that either population decreases or remains constant when the GDP has increased then the the growth in the per capita GDP will be higher because minute increases in the GDP will increase the answer with significant percentages.

Answer:

Ricardo’s Theory of Comparative Advantage

Explanation:

Comparative advantage is the term used to define the ability of an individual, firm or country to produce a particular good or service at a lower opportunity cost than that if it’s competitors or trade partners. Opportunity cost is the benefit lost from the second best alternative.

When a country can produce a product more efficiently (i.e maximum output using minimum resources) than that of its trade partners, it is known as that it has absolute advantage in that product. India tends to have absolute advantage in both business processes outsourcing as well as producing agricultural commodities as it is mentioned that it can produce both of these more efficiently than the United States.

However, although it has absolute advantage in both, it is still less efficient in producing agricultural commodities when compared to business process outsourcing. In other words, if it attempts to produce agricultural commodities in-house, the benefit lost from the second best alternative: business process outsourcing is high. The opportunity cost is higher when it produces agricultural commodities than it is when it does business process outsourcing. Hence, due to the law of comparative advantage, it chooses to specialize in business process outsourcing and imports agricultural commodities.

Operating cash flow = ($649,000 x .072) + $102,600 = $149,328. In financial accounting, operating cash flow or as called as OCF in which cash flow provided by operations, cash flow from operating activities or as called as CFO or free cash flow from operations or as called as FCFO bring up to the sum of cash a company produces from the revenues it brings in not including costs related with long-term investment on capital items.

Answer:

Debit Supplies expense $5,661

Credit Supplies account $5,661

Explanation:

At the time of purchasing supplies, the entries includes a debit to supplies accounts, and a credit to cash or accounts payable which is dependent on whether the cash purchased was done via cash or an account

For supplies used, debit supplies expense and credit supplies account. The movement in supplies account over a period is due to purchases and its expressed as;

Opening balance + Purchases - Supplies used = closing balance

$1,693 + $4,413 - Supplies used = $445

$6,106 - Supplies used = $445

Supplies used = $6,106 + $445

Supplies used = $5,661

I would suggest her to opt for scholarship programs that are offered by several colleges, there is a need based scholarship programs too.