r printer. The existing equipment has a current book value of $2,200,000 and a remaining life (if not replaced) of 10 years. The laser printer has a cost of $1,300,000 and an expected useful life of 10 years. The laser printer would increase the company’s annual cash flows by reducing operating costs and by increasing the company’s ability to gener- ate revenue. Susan Mills, controller of Metro Printers, has prepared the following estimates of the laser printer’s effect on annual earnings and cash flow:

Estimated increase in annual cash flows (before taxes):

Incremental revenue: 140,000

Cost savings (other than depreciation): 110,000

Reduction in annual depreciation expense:

Depreciation on existing equipment . . . . ......... 220,000

Depreciation on laser printer . . . . . . . . . . ......... 130,000

Estimated increase in income before income taxes . . . 340,000

Increase in annual income taxes (40%) . . . . . . . . . . . . . 136,000

Estimated increase in annual net income : ........................204,000

Estimated increase in annual net cash flows. . . . . . . . . . . 114,000

Don Adams, a director of Metro Printers, makes the following observation: "These estimates look fine, but won’t we take a huge loss in the current year on the sale of our existing equipment? After the invention of the laser printer, I doubt that our old equipment can be sold for much at all." In response, Mills provides the following information about the expected loss on the sale of the existing equipment:

Book value of existing printing equipment . . . . . . . . . . . . . . . . . . . . . . . . . . . .2,200,000

Estimated current sales price, net of removal costs . . . . . . . . . . . . . . . . . . . . . 200,000

Estimated loss on sale, before income taxes . . . . . . . . . . . . . . . . . . . . . . . . . .2,000,000

Reduction in current year’s income taxes as a result of loss (40%) . . . . . . . . . 800,000

Loss on sale of existing equipment, net of tax savings: 1,200,000

Adams replies, "Good grief, our loss would be almost as great as the cost of the laser itself. Add this $1,200,000 loss to the $1,300,000 cost of the laser, and we’re into this new equipment for $2,500,000. I’d go along with a cost of $1,300,000, but $2,500,000 is out of the question."

Instructions

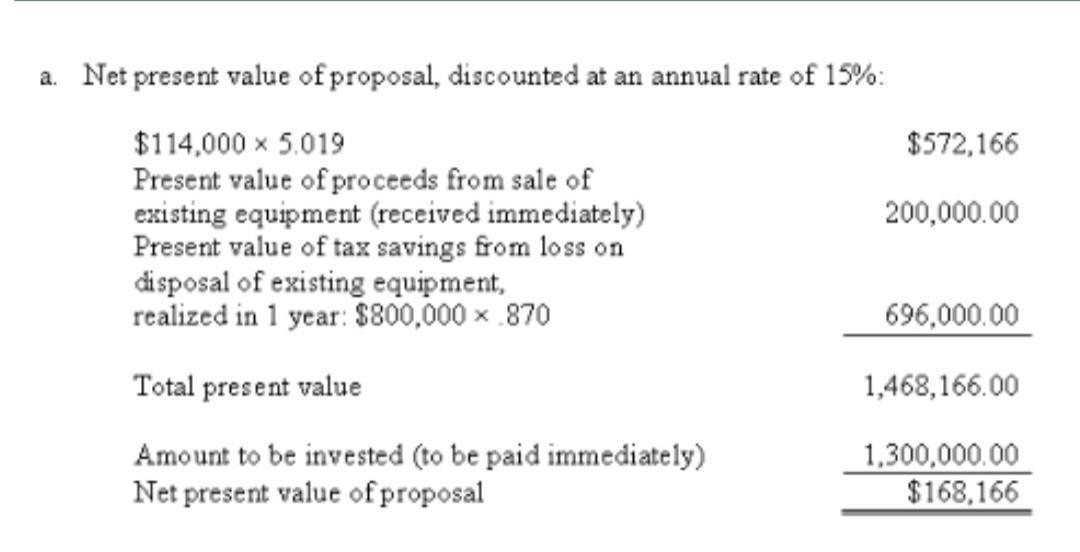

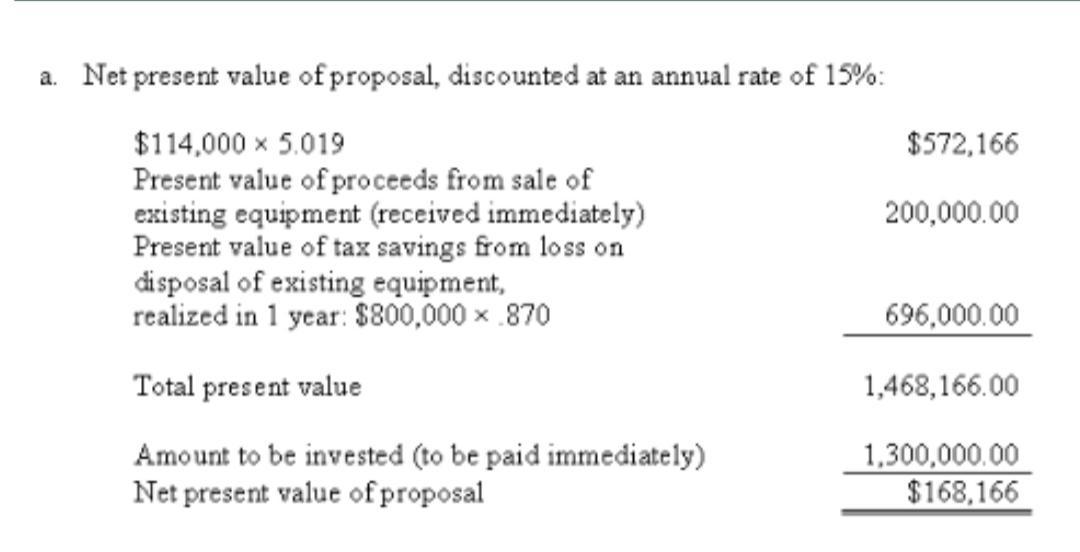

a. Use Exhibits 26–3 and 26–4 to help compute the net present value of the proposal to sell the existing equipment and buy the laser printer, discounted at an annual rate of 15 percent. In your computation, make the following assumptions regarding the timing of cash flows:

1. The purchase price of the laser printer will be paid in cash immediately.

2. The $200,000 sales price of the existing equipment will be received in cash immediately.

3. The income tax benefit from selling the equipment will be realized one year from today.

4. Metro uses straight-line depreciation in its income tax returns as well as its financial statements.

5. The annual net cash flows may be regarded as received at year-end for each of the next 10 years.

b. Is the cost to Metro Printers of acquiring the laser printer $2,500,000,