Answer: A - nominal wages are slow to adjust to changing economic conditions

Explanation:

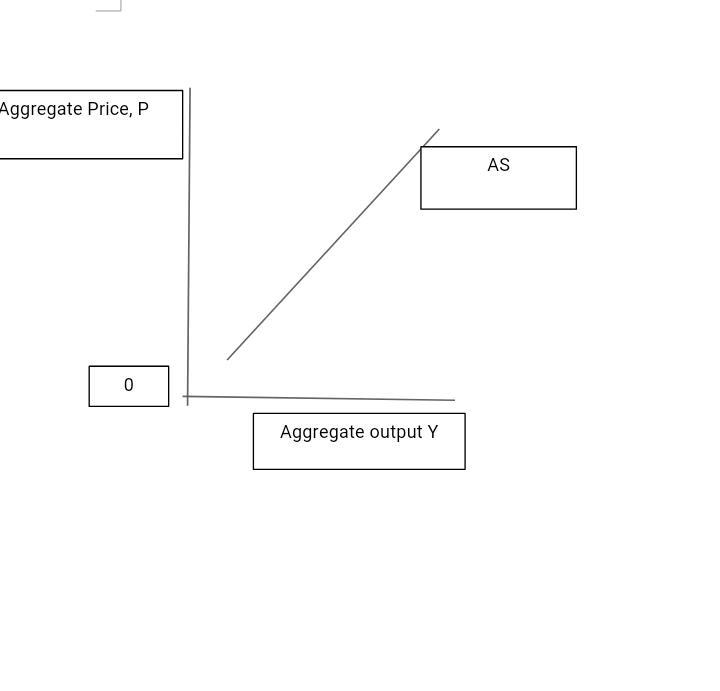

In the short run, the costs of many of the factors used in the production process are fixed. For example labours wage is fixed for a number of years because of labour contracts. Also the raw materials used in the production process have long term agreements that fix their prices.

As a result of factors of production been fixed in the short run, when general price level rises and the cost of production remains constant, profit also rises.

Firms take advantage of this rise in price and increase production and the quantity of aggregate supply increases. This is why the short run aggregate supply curve is upward sloping.

Answer:

B. $183,000

Explanation:

Calculation to determine The amount of cash that will be collected in July is budgeted to be

Budgeted collection in July = July sales (190,000*35%) + June sales (210,000*45%) + May sales (110,000*20%)

Budgeted collection in July =$66,500 +$94,500 + $22,000

Budgeted collection in July=$183,000

Therefore The amount of cash that will be collected in July is budgeted to be $183,000

Answer:

This question is incomplete. However, I found the prompt to be as follows;

"What is the productivity measure of “units of output per dollar of input” averaged over the four-year period? "

Explanation:

To solve this question, find productivity;

Productivity in this case is total hamburgers produced divided by the total labor cost plus total equipment cost.

Productivity = # of hamburgers *52 weeks * 4 years / (total labor cost + equipment cost)

Productivity= 40,000(52)(4)/ {9,500(4) + 5000}

= 193.5 hamburgers/dollar of input

Therefore, the factory would produce about 194 burgers per dollar of input.

Answer:

it a person that is in line to be the nexted manger

Explanation:

Answer:

1. An index determined by measuring the price of standard goods brought by urban consumers.

2. Producers raise prices to meet increased cost.

3. Demand-pull theory.

4. It rises

5. 4 percent.

Explanation: