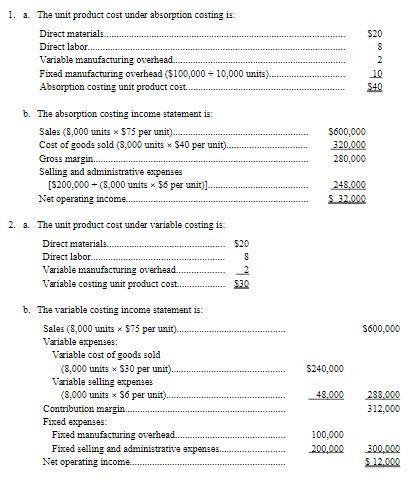

The difference in the ending inventory relates to a difference in the handling of fixed manufacturing overhead costs.

Under variable costing, these costs have been expensed in full as period costs.

Under absorption costing, these costs have been added to units of a product at the rate of $10 per unit ($100,000/10,000 units produced = $10 per unit).

Thus, under absorption costing a portion of the $100,000 fixed manufacturing overhead cost for the month has been added to the inventory account rather than expensed on the income statement:

Added to the ending inventory:

(2,000 units x $10 per unit) $ 20,000

Expensed as part of the cost of goods sold:

(8,000 units $10 per unit) $ 80,000

Total fixed manufacturing overhead cost for the month: $100,000

Because $20,000 of fixed manufacturing overhead cost has been deferred in inventory under absorption costing, the net operating income reported under that costing method is $20,000 higher than the net operating income under variable costing(refer to the first image)

And for question refer to the second image.

Hence, The difference in the ending inventory relates to a difference in the handling of fixed manufacturing overhead costs.

Learn more about absorption costing:

brainly.com/question/22079536

#SPJ4