Since you didn't give any methods to choose from, I will post several that can help a person recover their stolen goods. Contacting the police is the best way to recover your goods. A person should always write down serial numbers of their items such as electronics, guns, etc. The police should document and recover any physical evidence left at the crime scene. If you have jewelry in your home, you should always have a picture of all the jewelry to aid in the recovery. <span />

If labor in Mexico is less productive than labor in the united states in all areas of production then both Mexico and us still can benefit from trade.

Labor is the amount of physical, mental and social effort spent to produce goods and services in the economy. We provide the know-how, human resources, and services necessary to turn raw materials into finished products and services.

A business that requires more people and fewer machines is known as a labor-intensive business. The beauty, home construction, education and fashion industries are examples of labor-intensive industries.

Learn more about labor here:brainly.com/question/453055

#SPJ4

Answer:

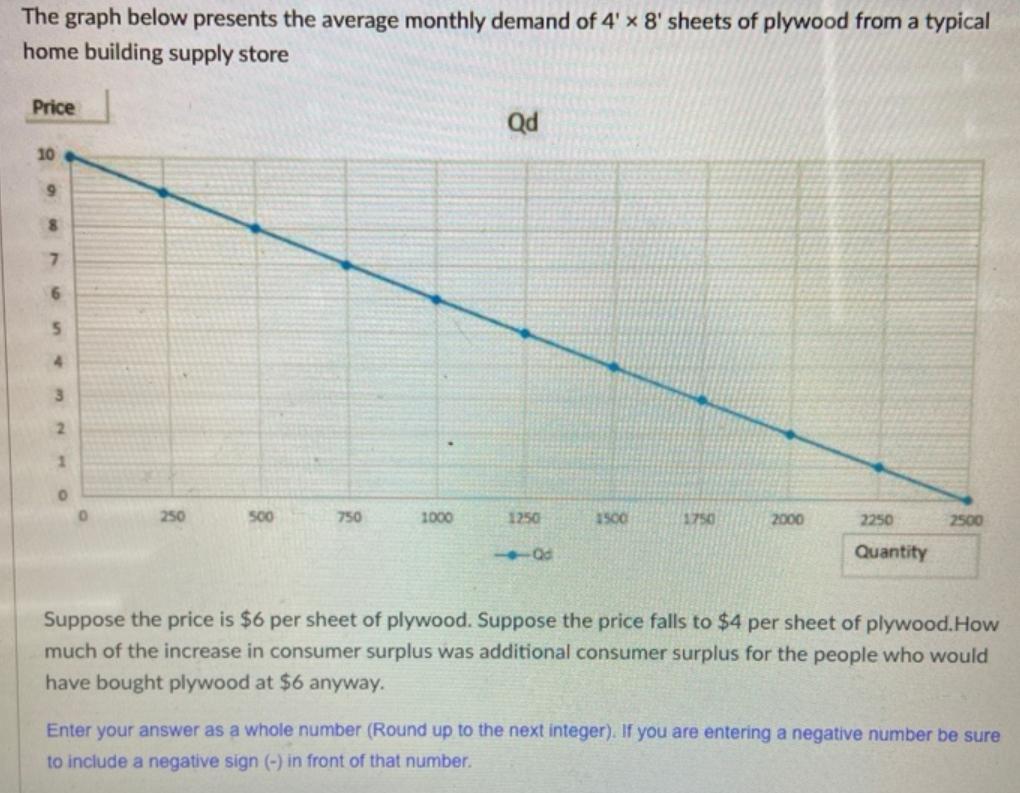

"$2,500" is the appropriate answer.

Explanation:

The question given seems to be incomplete. Below there is a attachment of full question is provided.

The given values are:

Plywood's price,

= $6 per sheet

Price falls,

= $4

Now,

At price $6, the consumer surplus will be:

=

=

=  ($)

($)

When price falls, the consumer surplus will be:

=

=

=  ($)

($)

Hence,

The increase in consumer surplus will be:

=

=  ($)

($)

Answer:

Under capitalistic economy, allocation of various resources takes place with the help of market mechanism. Price of various goods and services including the price of factors of production are determined with help of the forces of demand and supply. Free price mechanism helps producers to decide what to produce.

The goods which are more in demand and on which consumers can afford to spend more, are produced in larger quantity than those goods or services which have lower demand. The price of various factors of production including technology helps to decide production techniques or methods of production. Rational producer intends to use those factors or techniques which has relatively lower price in the market.

Factor earnings received by the employers of factors of production decides spending capacity of the people. This helps producers to identify the consumers for whom goods could be produced in larger or smaller quantities. Price mechanism works well only if competition exists and natural flow of demand and supply of goods is not disturbed artificially.

Explanation:

Answer:

pre-bonus income is $33600

Explanation:

given data

bonus = 20% of net income

income before the bonus = $57600

to find out

pre-bonus income

solution

we know pre income bonus is express as

pre-bonus income = bonous + share of income ............1

so bonus = 20/120 × 57600 = $9600

and share of net income = 1/2 × ( 57600 - 9600)

share of net income = $24000

so from equation 1

pre-bonus income = bonous + share of income

pre-bonus income =9600+ 24000

pre-bonus income is $33600