The feature of the insurance contract that is being described above is the aleatory contract. It is the type of contact where the individual that has been involved can't handle or control the event that could happen to him or her. It is a way of having uncertain events happening in the individual such as death or natural disasters that she or he could face.

A self-motivation was ablt to fit into the career readiness model because it is an attitude.

<h3>What is a

self-motivation?</h3>

It refers to the personal ability to motivate and drive oneself to take initiative and action to pursue set goals and complete tasks.

Therefore, the self-motivation was ablt to fit into the career readiness model because it is an attitude that is innate in an individual.

Read more about self motivation

<em>brainly.com/question/11871721</em>

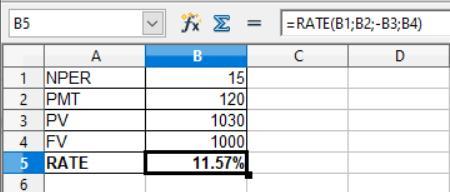

Answer:

11.57% and 9.02%

Explanation:

For computing the before-tax and after- tax cost of debt we use the RATE formula i.e to be shown in the attachment below:

Given that,

Present value = $1,050 - $20 = $1,030

Future value or Face value = $1,000

PMT = 1,000 × 12% = $120

NPER = 15 years

The formula is shown below:

= Rate(NPER;PMT;-PV;FV;type)

The present value come in negative

So, after solving this,

1. The pretax cost of debt is 11.57%

2. And, the after tax cost of debt would be

= Pretax cost of debt × ( 1 - tax rate)

= 11.57% × ( 1 - 0.22)

= 9.02%

Answer:

While it was true that the cotton gin reduced the labor of removing seeds, it did not reduce the need for slaves to grow and pick the cotton. In fact, the opposite occurred. Cotton growing became so profitable for the planters that it greatly increased their demand for both land and slave labor.

Monetarism in the AD-AS framework suggests that a decrease in velocity produces a leftward shift of the AD curve

<h3>What is

AD curve?</h3>

An aggregate demand curve (AD) depicts the relationship between total output demanded (measured in real GDP) and price level (measured as the implicit price deflator).

An aggregate demand curve depicts total domestic spending on goods and services at each price level. An example aggregate demand curve is shown below. The horizontal axis represents real GDP, and the vertical axis represents price level, as in an aggregate supply curve.

As aggregate demand components—consumption spending, investment spending, government spending, and spending on exports minus imports—increase, the aggregate demand curve, or AD curve, shifts to the right. As these components fall, the AD curve will shift back to the left.

To know more about AD curve follow the link:

brainly.com/question/17118208

#SPJ4