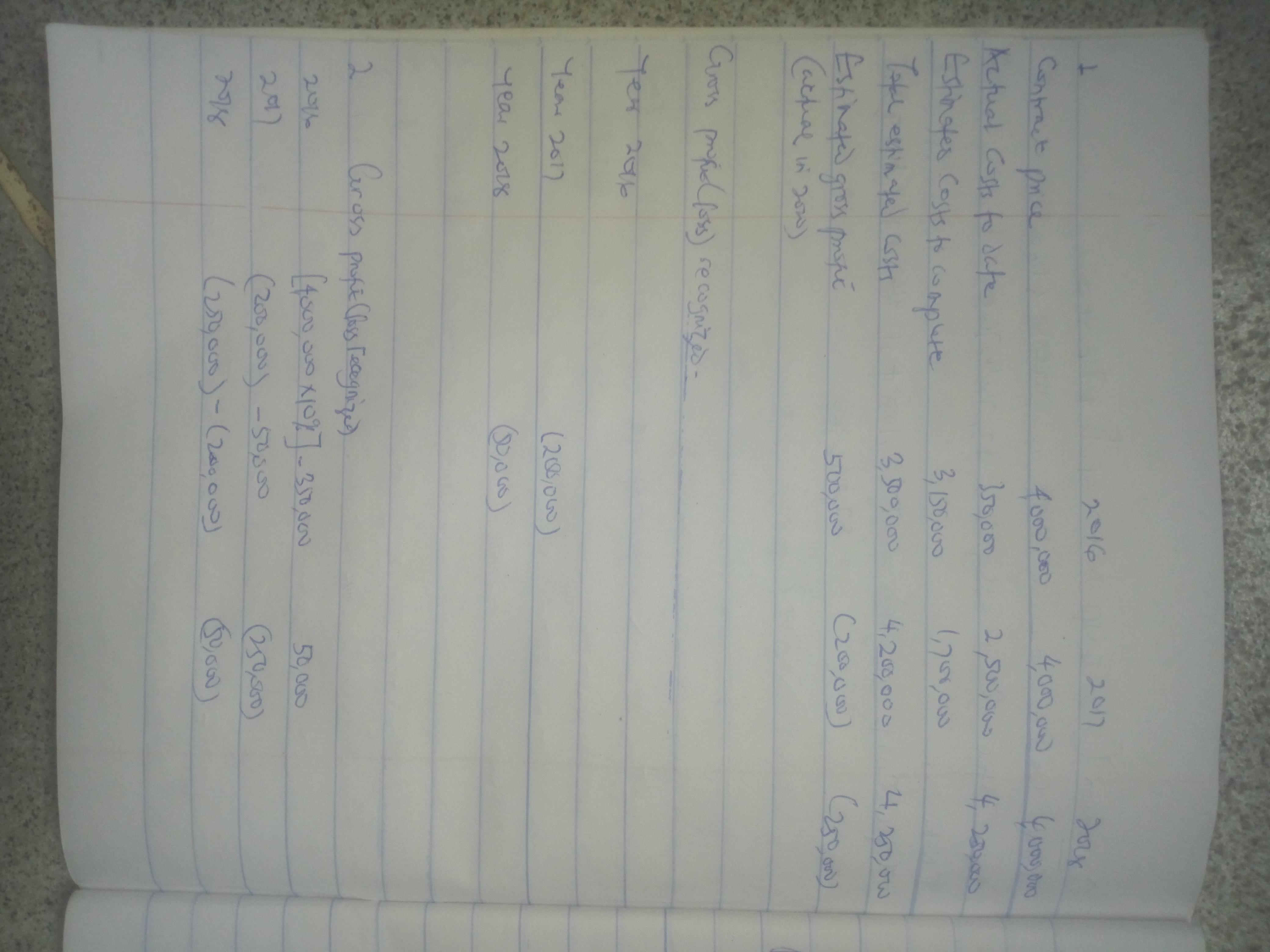

four-story office building. At that time, Curtiss estimated that it would take between two and three years to complete the project. The total contract price for construction of the building is $4,000,000. Curtiss concludes that the contract does not qualify for revenue recognition over time. The building was completed on December 31, 2018. Estimated percentage of completion, accumulated contract costs incurred, estimated costs to complete the contract, and accumulated billings to Axelrod under the contract were as follows:

At 12-31-2016 At 12-31-2017 At 12-31-2018

Percentage of completion 10% 60% 100%

Costs incurred to date $350,000 $2,500,000 $4,250,000

Estimated costs to complete 3,150,000 1,700,000 0

Billings to Axelrod, to date 720,000 2,170,000 3,600,000

Required:

1. Compute gross profit or loss to be recognized as a result of this contract for each of the three years.

Year Gross Profit (Loss) Recognized

2016

2017

2018

Total project profit (loss)

2. Assuming Curtiss recognizes revenue over time according to percentage of completion, compute gross profit or loss to be recognized in each of the three years.

Year Gross Profit (Loss) Recognized

2016

2017

2018

3. Assuming Curtiss recognizes revenue over time according to percentage of completion, compute the amount to be shown in the balance sheet at the end of 2016 and 2017 as either cost in excess of billings or billings in excess of costs.

Balance Sheet (Partial) 2016 2017

Current assets:

Current liabilities: