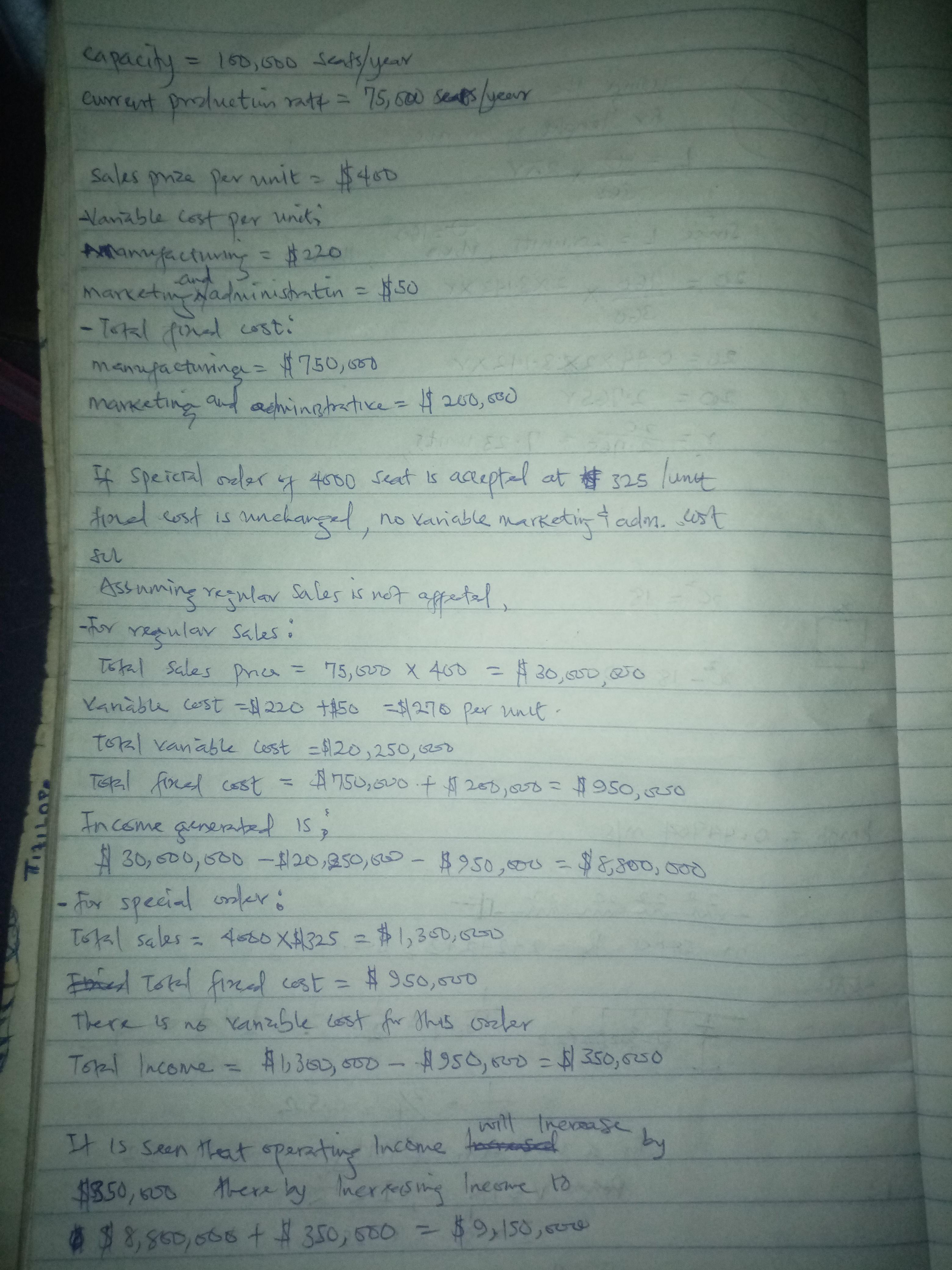

Answer:

The company's operating income will increase from $8,800,000 by $350,000 to become $9,150,000

Explanation:

Detailed explanation and calculation is shown in the image below

Answer:

C. Provided goods or services to a customer.

Explanation:

Book keeping is the act of recording financial transactions of a business on a day to day basis. The purpose is to keep concise and up-to-date record of the financial transactions.

Book keeping helps in analyzing finances, assist in planning and aids better decision making.

When revenue is recorded relating to a customer's transaction, it means that the company involved has provided goods or services to a customer. The recorded transaction is a proof of services provided and evidence that the transaction passed through the company's records.

The correct answer is A. Debit cards withdraw money directly from your account.

Explanations:

B. Debit cards offer less fraud protection than a credit card; the money has already left your hands whereas with credit cards it doesn't until the end of the month.

C. Debit cards do in fact require signatures. Yeah.

D. Debit cards charge much lower rates (if any, depending on the bank) because you are paying up front versus waiting until the end of the month when you will likely be charged interest and/or fees.

Hope I helped!

Refers to you having a job going hopefully this helped

Answer:

a. 12.60%

Explanation:

The information given above that can be useful is the Risk Free rate and risk premium to calculation of cost of retained earnings.

We know that the calculation of cost of retained earnings =Cost of retained earnings = Risk Free rate + risk premium

= 8.75% + 3.85%

= 12.6%

Therefore the correct answer is a. 12.60%