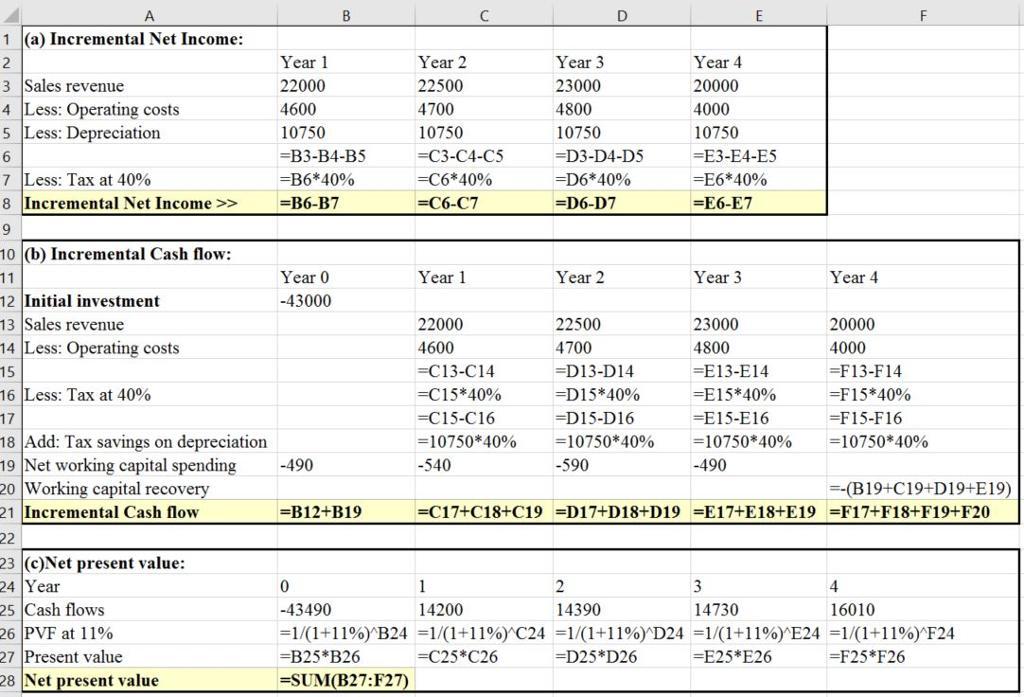

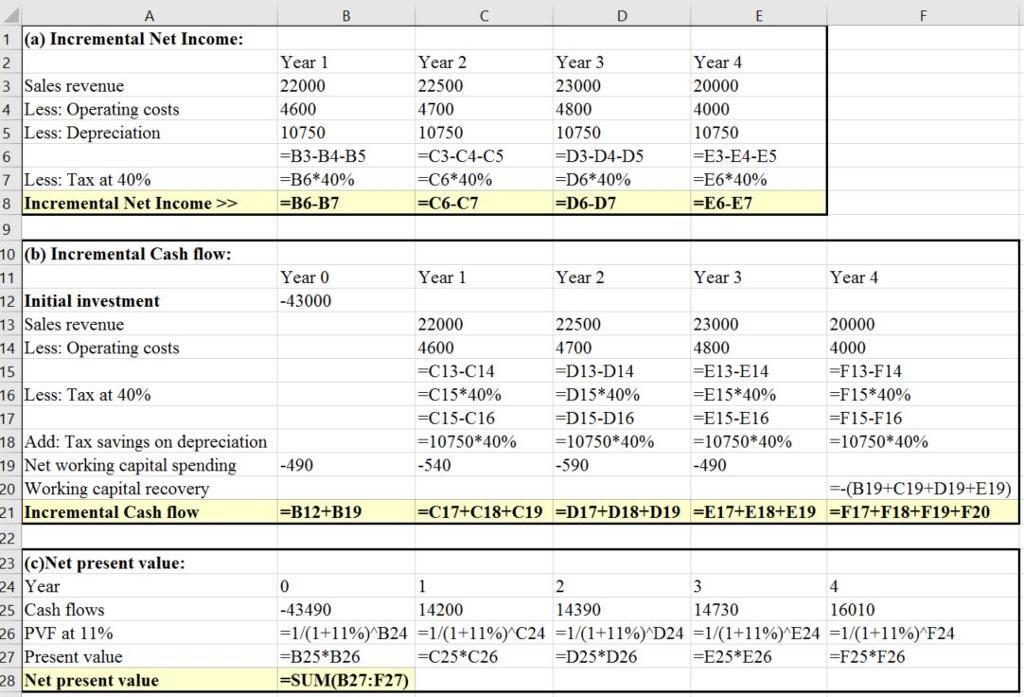

Answer: Net Present Value = 2576.09

Explanation:

Year 1 Year 2 Year 3 Year 4

Sales 22000 22500 23000 20000

Operating costs -4600 -4700 -4800 -4000

Depreciation -10750 -10750 -10750 -10750

Net working capital<u> -490 -540 -590 *1620

</u>

Profit before tax 6160 6510 6860 6780

**Income tax <u>-2464 -2604 -2744 -2748

</u>

Net income <u>3696 3906 4116 4122</u>

*net working capital costs recovered in year 4 = total net working capital expenses – Year 4 expense net working capital costs recovered in year 4 = (490 + 540 + 590 + 490) – 490 = 1620

** profit before tax multiplied by 40%

B. Incremental Cash Flows

Year 1 Year 2 Year 3 Year 4

Net income 3696 3906 4116 4122

Depreciation <u>10750 10750 10750 10750

</u>

Cash Flow <u>14446 14656 14866 14872

</u>

Depreciation is added back because it is a non cash item

C. Net present value

The Net present Value = Present Value of cash flows – initial investment

The Net present Value = 45576.09 – 43000 = 2576.09

Net Present Value = $ 2576.09