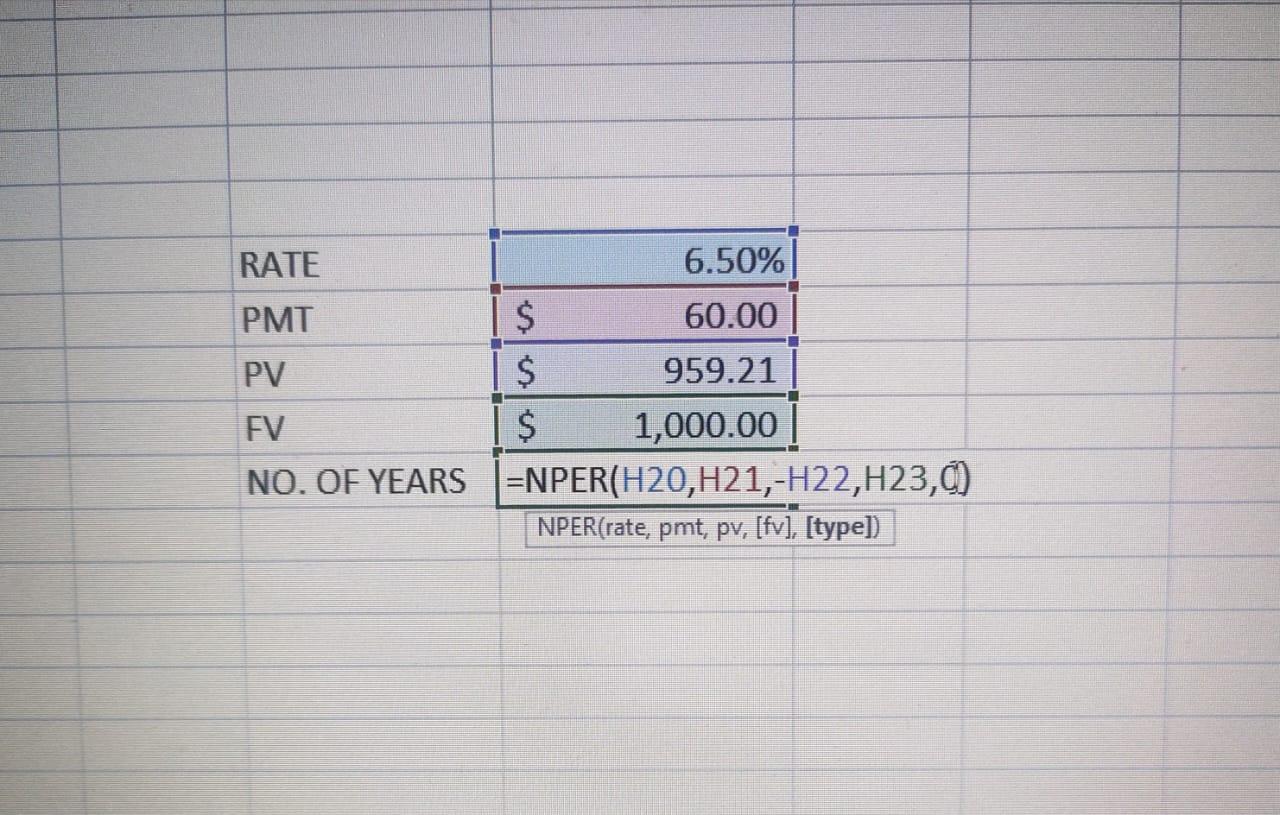

At the current interest rate of 6.5%, the bonds will mature in 12 years.

CALCULATIONS:

RATE= 6.5%

PMT= 1000$*6% = 60$

PV= 959.21$

FV= 1000$

NO. OF YEARS TO MATURE= NPER(rate, pmt, -pv,fv,0)

=NPER(6.5%,60$,-959.21$,1000$,0)

=12 YEARS

A coupon bond, also known as a bearer bond or bond coupon, is a debt obligation that includes semiannual interest coupons. The issuer keeps no record of coupon bond purchasers, and the purchaser's name is not printed on any kind of certificate. Between the time the bond is issued and the time it matures, bondholders receive these coupons.

Coupons are typically described in terms of the coupon rate, which is the yield paid on the date of issuance by a coupon bond. The interest rate on the coupon is subject to change. The coupon rate is calculated by adding all of the annual coupons and dividing the total by the bond's face value.

Learn more about coupon bonds here:

brainly.com/question/14746407

#SPJ4

Answer: $8,600

Explanation:

Implicit cost is also known as the opportunity cost which means that it is the benefit of the next best alternative that was foregone when the current decision was made.

The implicit cost here is therefore:

The $8,000 that Charles could have been making as a lifeguard.

The interest per year he could have been earning on the $5,000 he used to buy mowing equipment.

The depreciation on the mowing equipment because depreciation is not an explicit cost but an implicit one.

= 8,000 + (2% * 5,000) + (10% * 5,000)

= 8,000 + 100 + 500

= $8,600

Answer:

the right answer is A.

Explanation:

because Those responsible for ensuring the health and safety of their workers are the professionals who study the regulation of these standards

Answer:

Tragedy of the commons.

Explanation:

The "Tragedy of the Commons" refers to the phenomenon where People overuse a common resource. It is a situation arise when individual user share resources with much other and demand increase in comparison to the supply of resources, which lead to depletion, destruction, or damage to resources due to overconsumption. It can be prevented by using certain measures like fixing ownership of resources, assigning basic rules and regulations for usage of resources, penalizing for damage, etc.

In the given case, a retired athlete built a gym and made it common and free for neighborhood residents, which lead to overuse of gym facility and that is a tragedy of common arise.

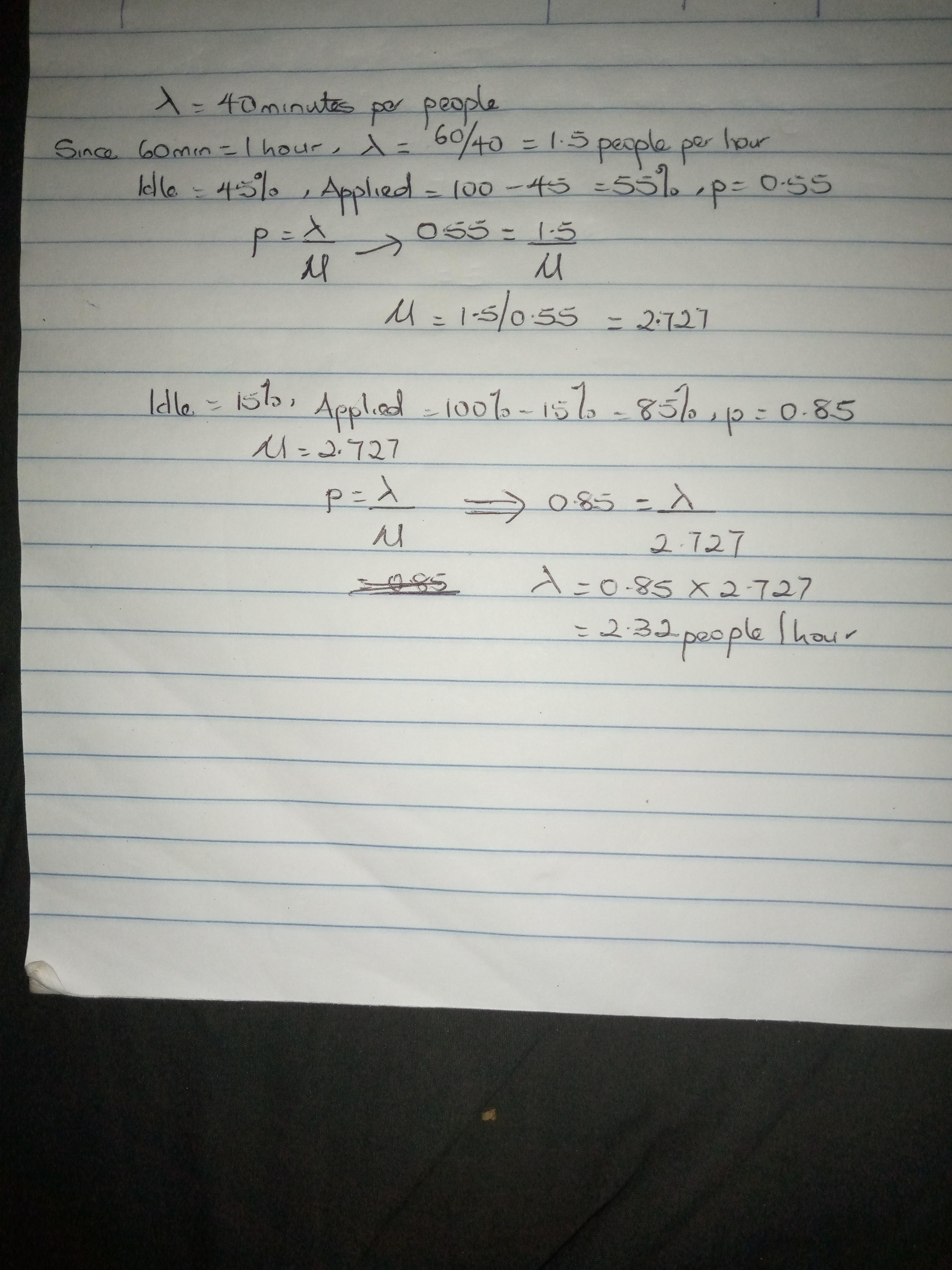

Answer: 2.32 people per hour

Explanation:

From the question, we are informed that Bobby the Barber is thinking about advertising in the local newspaper since he is idle 45 percent of the time and that currently, customers arrive on average every 40 minutes.

For Bobby to be busy 85 percent of the time, the arrival time needs to be 2.32 people per hour.

Check the attached file for the solution.